Borrowing crypto without understanding collateral ratios is like driving without knowing your fuel gauge. You might feel fine right up until everything stops working. The number that determines whether you keep your assets or lose them to liquidation isn’t complicated, but getting it wrong costs people thousands every single day.

Collateral ratio DeFi measures how much crypto you lock up versus what you borrow. Most protocols require 150% or higher, meaning you deposit $150 to borrow $100. This buffer protects against price drops. If your ratio falls below the minimum threshold, the protocol automatically liquidates your collateral to repay the loan. Understanding and monitoring this number is the single most important skill for safe DeFi borrowing.

What collateral ratio actually means in DeFi

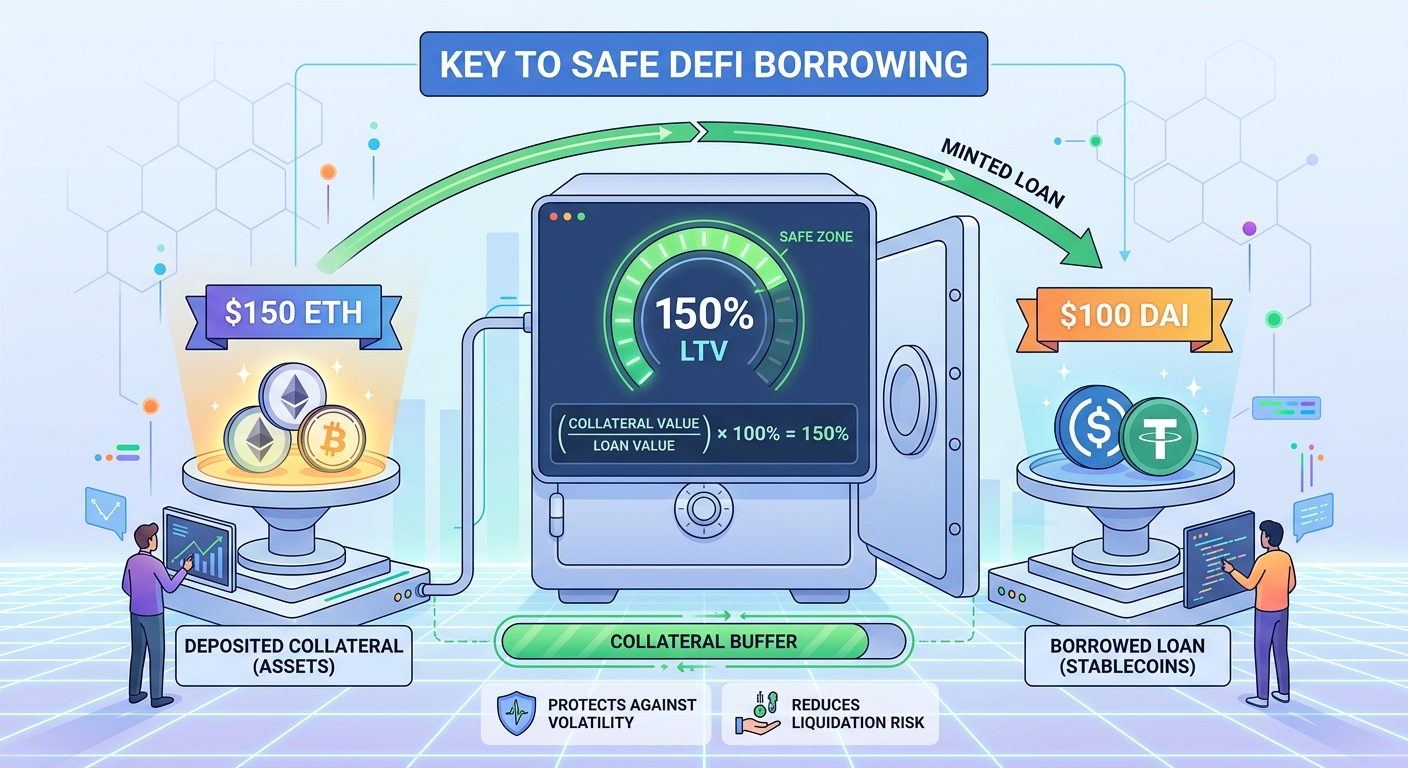

Your collateral ratio is the percentage relationship between what you deposit and what you borrow.

The formula looks like this: (Collateral Value / Borrowed Value) × 100 = Collateral Ratio.

If you deposit $1,500 worth of ETH and borrow $1,000 in stablecoins, your ratio sits at 150%. The protocol considers this your safety margin.

Different platforms set different minimum requirements. Aave might accept 125% for certain assets. MakerDAO typically requires 150% or higher. Compound varies by token type.

These aren’t arbitrary numbers. They reflect how volatile each asset tends to be.

Bitcoin might get a lower requirement because it’s relatively stable. A newer altcoin might demand 200% or more because its price swings wildly.

The protocol doesn’t care about your intentions. It only watches the math. When your ratio drops below the threshold, automated systems take over.

Why protocols demand over-collateralization

Traditional banks let you borrow $200,000 with a $40,000 down payment on a house. That’s 20% collateral.

DeFi flips this completely.

You need to deposit more than you borrow because smart contracts can’t chase you for payment. There’s no credit score. No legal system backing the loan. No way to garnish your wages.

The only guarantee the protocol has is the crypto sitting in the contract right now.

Price volatility makes this even more critical. Your ETH collateral might drop 15% in an afternoon. The protocol needs enough cushion to sell your collateral and recover the full loan amount before the value disappears.

How does DeFi actually work without banks or middlemen? explains why this trustless system requires such different rules than traditional finance.

Over-collateralization protects both sides. You get to borrow without permission. The protocol gets certainty it can recover funds.

How liquidation actually happens

Liquidation isn’t a punishment. It’s an automatic safety mechanism.

Here’s the exact sequence:

- Your collateral value drops or your debt increases (through interest)

- Your ratio falls below the protocol’s minimum threshold

- The smart contract flags your position for liquidation

- Liquidators (specialized bots or users) repay part or all of your debt

- They receive your collateral at a discount as a reward

- You lose your collateral but the debt is cleared

Most protocols don’t liquidate everything at once. They might liquidate just enough to bring your ratio back above the minimum.

The liquidation penalty varies. Aave charges around 5% to 10%. Other platforms might take 13% or more.

This penalty goes to the liquidator as an incentive. Without this reward, nobody would bother monitoring positions and executing liquidations.

Speed matters enormously. In a market crash, your position might go from healthy to liquidated in minutes. Manual intervention rarely works fast enough.

Calculating your safe borrowing limit

Start with your collateral value. Let’s say you have $10,000 in ETH.

The protocol requires 150% collateral ratio minimum. But borrowing right at the minimum is dangerous.

Here’s the math for maximum borrowing at 150%:

– Maximum Borrow = Collateral Value / 1.5

– $10,000 / 1.5 = $6,666

But you shouldn’t borrow the maximum. Ever.

A 200% ratio gives you breathing room:

– Safe Borrow = $10,000 / 2 = $5,000

At 250%, you’re even safer:

– Conservative Borrow = $10,000 / 2.5 = $4,000

The higher your ratio, the bigger the price drop you can survive. With a 200% ratio, your collateral can drop 25% before you hit the 150% liquidation threshold.

How to calculate your liquidation price before taking a DeFi loan walks through the exact formulas for different scenarios.

Common mistakes that trigger liquidation

| Mistake | Why It Happens | How to Avoid It |

|---|---|---|

| Borrowing at maximum ratio | Trying to maximize capital efficiency | Always maintain 200% minimum ratio |

| Ignoring accruing interest | Debt grows while you’re not watching | Check positions daily during volatility |

| Using volatile collateral | Chasing high yields with risky tokens | Stick to major assets for large loans |

| No price alerts | Assuming you’ll notice problems | Set alerts at 175% and 160% ratios |

| Forgetting about gas fees | Can’t add collateral when fees spike | Keep emergency ETH in your wallet |

The worst mistake is borrowing and forgetting. Your ratio doesn’t stay static.

Interest accumulates on your debt. Even with stable collateral prices, your ratio slowly decreases. A position that starts at 200% might drift to 180% over weeks without any price movement.

Market volatility accelerates everything. A 20% ETH price drop combined with growing debt can push you into liquidation territory within hours.

Managing your ratio during market swings

Active monitoring separates successful borrowers from liquidated ones.

Set up multiple alert levels:

- Green zone (200%+): Comfortable. Check weekly.

- Yellow zone (175% to 199%): Caution. Check daily.

- Orange zone (160% to 174%): Danger. Consider adding collateral.

- Red zone (below 160%): Emergency. Act immediately.

You have three options when your ratio drops:

Add more collateral. Deposit additional crypto to boost your ratio. This is usually the safest choice if you have available funds.

Repay part of the debt. Reduces what you owe, improving your ratio. Good if you have stablecoins available.

Do nothing and accept liquidation risk. Sometimes the right move if you believe a dip will recover quickly. Extremely risky.

During the May 2021 crash, ETH dropped 40% in days. Positions with 150% ratios got liquidated. Those maintaining 200%+ survived.

What happens during a DeFi liquidation and how to avoid it covers real examples and survival strategies.

Different ratio requirements across protocols

Each platform sets its own rules based on risk tolerance and asset types.

MakerDAO (DAI loans):

– ETH collateral: 150% minimum

– More volatile assets: 175% or higher

– Conservative approach prioritizes stability

Aave:

– Varies by asset from 125% to 180%

– Uses health factor instead of simple ratio

– More aggressive liquidation triggers

Compound:

– Collateral factors range from 50% to 90%

– Different calculation method than other platforms

– Multiple assets can be combined

Liquity:

– 110% minimum ratio

– Much riskier but more capital efficient

– Recovery mode kicks in during market stress

The protocol you choose dramatically affects your liquidation risk. A 150% position on MakerDAO has more buffer than a 150% position on Liquity because of how liquidations trigger.

Why stablecoin collateral changes everything

Using USDC or DAI as collateral eliminates price volatility risk.

Your ratio stays almost perfectly stable. The only change comes from interest accumulation on your debt.

This sounds perfect, but there’s a catch. Borrowing stablecoins against stablecoin collateral doesn’t make much sense. You’re locking up $150 to borrow $100 of the same thing.

The real use case is borrowing different assets. Lock up USDC, borrow ETH to go long. Your liquidation risk now depends on ETH’s price going up, not down.

Some advanced users create delta-neutral positions. They balance long and short positions so price movements cancel out. This requires sophisticated strategy and constant monitoring.

USDT vs USDC vs DAI: which stablecoin should beginners trust? helps you pick the right stablecoin for collateral.

Interest rates and their hidden impact on ratios

Your debt doesn’t stay constant. It grows.

Variable rates change based on utilization. When lots of people borrow an asset, rates spike. Your debt accumulates faster.

Fixed rates lock in your cost but usually start higher than variable rates. You trade certainty for expense.

Here’s what many borrowers miss: even small interest rates compound over time.

A $10,000 loan at 5% APY costs you $500 in year one. But that interest gets added to your principal. Year two, you’re paying interest on $10,500.

Your collateral ratio drops as debt grows, even if your collateral value stays perfectly flat.

Check your actual debt amount, not just your original borrow amount. Protocols show both numbers, but people often focus on what they initially borrowed.

Variable vs fixed interest rates in DeFi lending: which should you choose? breaks down the trade-offs in detail.

Multi-collateral positions and ratio complexity

Some protocols let you deposit multiple asset types as collateral.

This creates complicated ratio calculations. Your ETH might be worth $5,000. Your BTC worth $3,000. Your total collateral is $8,000.

But each asset has different liquidation thresholds. ETH might allow 150% while BTC requires 140%.

The protocol calculates a weighted average based on what you’ve deposited. This composite ratio determines your liquidation risk.

Adding more collateral types increases complexity. You need to track multiple price feeds and understand how each asset affects your overall position.

Beginners should stick to single-collateral positions until they fully grasp the mechanics.

Real examples of ratio management

Conservative approach: Sarah deposits $20,000 in ETH. She borrows $8,000 in USDC. Her ratio starts at 250%.

ETH drops 30%. Her collateral is now worth $14,000. Her ratio falls to 175%. Still safe, but she adds $3,000 more ETH to boost back to 212%.

Aggressive approach: Mike deposits $15,000 in ETH. He borrows $10,000 in USDC. His ratio starts at 150%.

ETH drops 10%. His collateral is now $13,500. His ratio drops to 135%. He gets liquidated, losing roughly $1,500 in penalties plus his collateral.

Balanced approach: Jennifer deposits $30,000 in ETH. She borrows $12,000 in USDC. Her ratio starts at 250%.

She sets alerts at 200% and 175%. When ETH drops and triggers her 200% alert, she repays $2,000 of debt, bringing her ratio back to 225%.

The difference between these outcomes isn’t luck. It’s planning and discipline.

Tools and dashboards for tracking ratios

Don’t rely on memory or manual calculations.

DeFi Saver: Automated protection that adds collateral or repays debt when ratios drop. Costs fees but prevents liquidation.

Zapper: Portfolio dashboard showing all your positions across protocols. Updates in real time.

DeBank: Similar to Zapper with clean interface and mobile alerts.

Protocol native dashboards: Aave, Compound, and others show your health factor and ratio directly in their interface.

Custom alerts: Set up notifications through your wallet or third-party services. Get texts or emails when ratios hit danger zones.

Automation removes emotion from decisions. When your ratio drops to 165% at 3 AM during a flash crash, automated systems can save you.

Manual intervention often fails because you’re asleep, busy, or panicking.

Building your personal risk tolerance

Your acceptable ratio depends on several factors.

Market outlook: Bullish on your collateral? You might accept a lower ratio. Uncertain? Keep it high.

Loan duration: Borrowing for two days? 175% might be fine. Borrowing for six months? 250% is safer.

Monitoring ability: Check positions hourly? You can run tighter ratios. Check weekly? You need bigger buffers.

Asset volatility: ETH and BTC are relatively stable. Altcoins swing wildly. Adjust ratios accordingly.

Financial cushion: Can you add collateral quickly if needed? Then moderate ratios work. No backup funds? Stay conservative.

“I learned about collateral ratios the hard way. Lost $4,000 in a liquidation because I borrowed at 155% and didn’t set alerts. Now I never go below 200% and I sleep better.” — Alex, DeFi user since 2020

Start conservative. You can always borrow more later. You can’t undo a liquidation.

When borrowing doesn’t make sense

Sometimes the best decision is not borrowing at all.

If you need to lock up $15,000 to borrow $10,000, consider whether you actually need that $10,000. Selling $10,000 of your crypto might be smarter.

The math only works if you’re confident your collateral will appreciate more than your borrowing costs.

Example: You lock ETH worth $20,000. You borrow $10,000 at 5% APY. That’s $500 in yearly interest.

If ETH gains 30%, your collateral is now worth $26,000. You made $6,000 minus $500 in interest. Net gain of $5,500.

If ETH drops 30%, your collateral is worth $14,000. You still owe $10,500 (with interest). You’re approaching liquidation and might lose everything.

How to borrow crypto without selling your assets helps you decide when borrowing beats selling.

Protecting yourself from ratio-related scams

Scammers exploit confusion around collateral ratios.

Fake liquidation warnings: Phishing emails claiming your position is about to liquidate. They link to fake protocol sites that steal your wallet credentials.

Guaranteed ratio protection services: Promises to maintain your ratio for a fee, then disappear with your funds.

Too-good-to-be-true ratios: New protocols offering 50% collateral requirements. Usually exit scams waiting to happen.

Always verify liquidation status directly through the official protocol website. Never click email links.

Legitimate protocols never ask for your private keys or seed phrase to “protect your ratio.”

5 free tools to check if a DeFi protocol is safe shows you how to verify protocol legitimacy before depositing.

Your ratio strategy checklist

Before opening any collateralized position:

- Calculate your maximum safe borrow amount at 200% minimum ratio

- Set up price alerts at 200%, 175%, and 160% ratios

- Verify you have emergency funds to add collateral if needed

- Understand the protocol’s exact liquidation threshold and penalty

- Check current interest rates and factor growth into your planning

- Test with a small position first to understand the interface

- Document your liquidation price and check it daily

- Know exactly how to add collateral or repay debt quickly

This checklist takes 15 minutes. Skipping it costs thousands.

Making collateral ratios work for you

Understanding collateral ratio DeFi isn’t about memorizing formulas. It’s about respecting the math that protects your assets.

The protocols don’t care about your story. They execute code. When your ratio hits the threshold, liquidation happens automatically.

But this isn’t a weakness. It’s actually the strength of DeFi. No human can decide to liquidate you unfairly. No bank can change the rules mid-loan.

You just need to play by the rules that are clearly visible from the start.

Start conservative. Monitor actively. Build experience with small positions. Graduate to larger loans only after you’ve successfully managed ratios through at least one period of market volatility.

Your first successful loan that survives a 20% price swing teaches you more than any article ever could. That’s when the numbers transform from abstract concepts into tools you genuinely understand and control.