You’ve probably seen those eye-popping APY numbers advertised on DeFi platforms. 8%, 12%, sometimes even 20% annual returns just for depositing your stablecoins. It sounds too good to be true, especially when traditional savings accounts barely offer 0.5%. But here’s the thing: earning interest on stablecoins through DeFi lending is real, and thousands of people do it every day. The question isn’t whether it works. The question is whether you understand what you’re actually doing with your money.

You can legitimately earn interest on stablecoins through DeFi lending platforms by depositing your funds into liquidity pools that borrowers use. Typical realistic yields range from 3% to 10% APY, depending on the platform and market conditions. The interest comes from real borrowers paying fees, not magic. However, you face smart contract risks, platform insolvency, stablecoin de-pegging, and regulatory uncertainty that traditional banks don’t present.

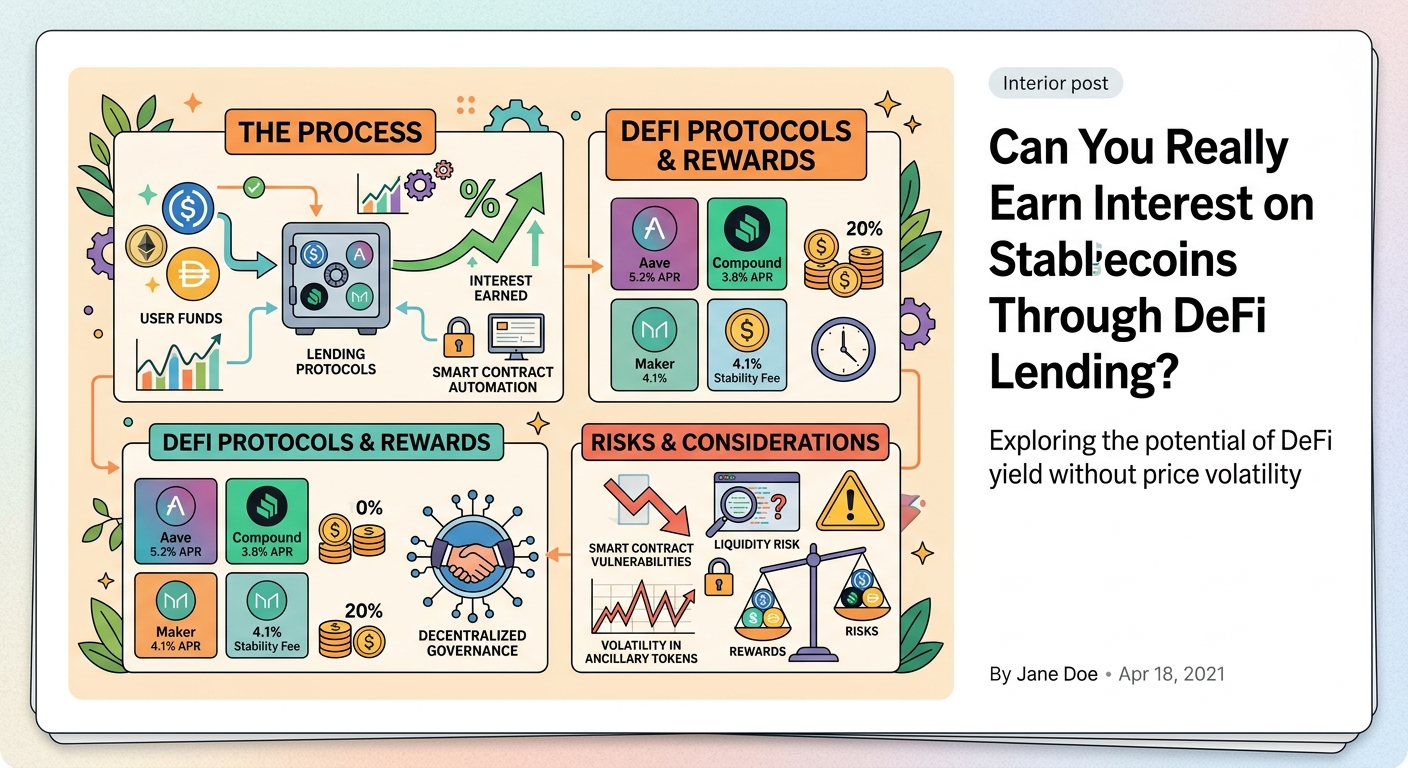

How stablecoin interest actually works in DeFi

When you deposit stablecoins into a DeFi lending protocol, you’re not putting money into a bank vault.

You’re contributing to a liquidity pool.

Think of it like this: borrowers need stablecoins for various reasons. Maybe they want to leverage their crypto holdings without selling. Maybe they need liquidity for arbitrage trading. They come to DeFi platforms, put up collateral (usually more than they borrow), and take out loans.

Your stablecoins sit in that pool, ready to be borrowed.

When someone borrows your stablecoins, they pay interest. That interest gets distributed to everyone who deposited funds into the pool, proportional to their share.

The protocol handles everything automatically through smart contracts. No loan officers. No credit checks. No paperwork.

How does DeFi actually work without banks or middlemen explains the underlying mechanics if you want to understand the technical foundation.

Here’s the basic process:

- You connect your wallet to a DeFi lending platform

- You approve the smart contract to access your stablecoins

- You deposit your stablecoins into the lending pool

- The protocol issues you receipt tokens representing your deposit

- Interest accrues automatically, often visible in real-time

- You can withdraw anytime (assuming there’s enough liquidity)

The interest rates aren’t fixed. They fluctuate based on supply and demand. When lots of people want to borrow and few are lending, rates go up. When everyone’s depositing and nobody’s borrowing, rates drop.

Where the yields actually come from

The interest you earn isn’t conjured from thin air.

It comes from three main sources:

Borrower interest payments make up the bulk of your returns. Borrowers pay interest rates that are typically higher than what lenders receive. The difference covers protocol operations and risk buffers.

Protocol incentives sometimes supplement yields. Some platforms distribute their governance tokens to lenders as an additional reward. This boosts your effective APY, but those token prices can be volatile.

Liquidation fees contribute smaller amounts. When borrowers fail to maintain their collateral ratios and get liquidated, a portion of the liquidation penalty sometimes flows back to lenders.

Let’s break down a realistic example:

| Yield Component | Typical Contribution | Stability |

|---|---|---|

| Base borrower interest | 3-7% APY | Moderate |

| Protocol token rewards | 0-5% APY | Volatile |

| Liquidation fees | 0-1% APY | Irregular |

| Total potential yield | 3-13% APY | Variable |

The platforms advertising 20%+ APY are usually offering temporary promotional rates or including highly volatile token rewards. Those numbers rarely last.

Understanding why DeFi yields are high and what risks you’re actually taking helps you evaluate whether advertised rates make sense.

Choosing between different stablecoin types for lending

Not all stablecoins are created equal for earning interest.

Your choice affects both your yield and your risk profile.

Fiat-backed stablecoins like USDC and USDT typically offer moderate yields (3-8% APY). They’re backed by real dollars in bank accounts, which makes them more stable but also more centralized. If the issuing company faces problems, your stablecoin could lose its peg.

Crypto-collateralized stablecoins like DAI usually offer slightly higher yields (4-10% APY) because they carry more complexity. They’re backed by other cryptocurrencies locked in smart contracts. More decentralized, but more moving parts.

Algorithmic stablecoins sometimes advertise the highest yields, but they’re also the riskiest. Remember Terra/Luna? That’s what happens when algorithmic mechanisms fail catastrophically.

For beginners, stick with USDC or DAI on established platforms.

USDT vs USDC vs DAI: which stablecoin should beginners trust provides a detailed comparison of the major options.

Here’s what to check before depositing:

- Does the stablecoin maintain its $1 peg consistently?

- Who issues it and what backs it?

- How long has it existed without major incidents?

- What’s the trading volume and liquidity?

- Are there regular attestations or audits of reserves?

The major platforms where you can earn interest on stablecoins

Several established platforms dominate the DeFi lending space.

Each has different features, risks, and yield structures.

Aave is one of the largest and most battle-tested protocols. It offers variable and stable interest rates, strong security audits, and a wide range of supported assets. Typical USDC yields range from 2-6% APY depending on market conditions.

Compound pioneered the autonomous interest rate protocol model. It’s simple, transparent, and has operated since 2018 without major exploits. Yields are usually slightly lower than competitors but more stable.

Curve Finance specializes in stablecoin swaps and offers competitive lending yields through its pools. It’s particularly efficient for stablecoin-to-stablecoin activities.

Maker lets you deposit DAI (which you might have borrowed against crypto collateral) and earn the DAI Savings Rate, currently around 3-5% APY. It’s the most decentralized option but offers lower yields.

Comparing platforms requires looking beyond headline APY numbers:

- What’s the protocol’s total value locked (TVL)?

- How many audits has it undergone?

- What’s its track record during market stress?

- How quickly can you withdraw during high demand?

- What are the gas fees for deposits and withdrawals?

5 best DeFi lending platforms for passive income in 2024 offers current platform comparisons.

Before depositing significant funds, start with a small test amount. Deposit, wait a few days, then withdraw. This helps you understand the process and identify any friction points before committing larger sums.

The real risks you’re accepting when you lend stablecoins

This is where most beginners underestimate what they’re getting into.

Traditional bank deposits come with FDIC insurance up to $250,000. DeFi lending has no such safety net.

Smart contract risk tops the list. Even audited code can contain bugs. If someone exploits a vulnerability in the lending protocol, your funds could disappear. It’s happened before, and it’ll happen again.

Stablecoin de-pegging risk is real. If your stablecoin loses its $1 peg, you might earn 8% APY but lose 20% of your principal value. What happens when stablecoins lose their peg? Real examples explained shows historical cases.

Platform insolvency risk exists even in DeFi. If a platform can’t meet withdrawal demands during a crisis, you might face delays or losses. This isn’t theoretical; it happened with Celsius and BlockFi in 2022 (though those were CeFi, not DeFi).

Regulatory risk is growing. Governments worldwide are scrutinizing DeFi lending. Future regulations could freeze platforms, require KYC, or restrict access entirely.

Oracle manipulation risk affects platforms that rely on price feeds. If someone manipulates the oracle, it could trigger false liquidations or other protocol malfunctions.

Here’s a risk comparison:

| Risk Type | Probability | Potential Impact | Mitigation Strategy |

|---|---|---|---|

| Smart contract bug | Low to Medium | Total loss | Use audited protocols, diversify |

| Stablecoin de-peg | Low | Partial loss | Choose established stablecoins |

| Platform insolvency | Low | Partial to total loss | Check TVL and track record |

| Regulatory action | Medium | Access restriction | Stay informed, have exit plan |

| User error | Medium | Total loss | Practice with small amounts first |

The complete DeFi security checklist for beginners provides a comprehensive safety framework.

How to start earning interest on stablecoins safely

If you’ve decided the yields justify the risks, here’s how to begin responsibly.

Start small. Really small.

Your first deposit should be an amount you’re comfortable losing entirely while you learn the system. $100 is plenty for testing.

Step 1: Set up a proper wallet

You need a non-custodial wallet like MetaMask or Rainbow. Don’t use an exchange wallet for DeFi activities. You need direct control.

5 critical mistakes beginners make when setting up their first DeFi wallet helps you avoid common setup errors.

Step 2: Acquire stablecoins

Buy USDC or DAI on a reputable exchange, then transfer them to your wallet. Start with one stablecoin type to keep things simple.

Step 3: Research your platform

Choose one established platform. Read recent reviews. Check the protocol’s status page. Look for any recent exploits or issues.

Step 4: Understand the interface before connecting

Most platforms have demo modes or documentation. Spend 30 minutes understanding how deposits, withdrawals, and interest tracking work.

Step 5: Make your first deposit

Connect your wallet. The platform will ask you to approve the smart contract. This is normal but understand what happens when you approve a smart contract.

Deposit your test amount. Watch how the interface updates. Note your receipt tokens.

Step 6: Monitor and learn

Check your position daily for the first week. Watch how interest accrues. Notice how APY fluctuates.

Step 7: Test withdrawal

After a week or two, withdraw your funds. Make sure you understand the process completely.

Only after successfully completing this cycle should you consider larger deposits.

Common mistakes that cost beginners money

Even experienced crypto users make errors when they start DeFi lending.

Chasing the highest APY is the number one mistake. That 25% yield on a new platform? It’s probably unsustainable and potentially dangerous. Stick with established protocols offering realistic rates.

Ignoring gas fees can eat your profits. If you’re depositing $200 and paying $50 in Ethereum gas fees, you need to keep funds deposited for months just to break even. Consider are layer 2 solutions finally making DeFi affordable for everyone for cheaper alternatives.

Not tracking tax implications creates problems later. In most jurisdictions, your interest earnings are taxable income. Keep records of deposits, withdrawals, and accrued interest.

Leaving unlimited approvals exposes you to risk. When you approve a smart contract, you often grant unlimited access to your tokens. Regularly review and revoke unnecessary approvals.

Putting all funds in one platform concentrates risk. If that protocol gets exploited, you lose everything. Diversify across 2-3 established platforms.

Forgetting about opportunity cost matters. If you can earn 4% in a DeFi protocol but you’re paying 18% on credit card debt, you’re making a mistake. Pay off high-interest debt first.

Not having an exit strategy leaves you vulnerable. Know exactly how you’ll withdraw if something goes wrong. Have you tested the withdrawal process? Do you know how long it takes? What if the interface is down?

Comparing DeFi lending returns to traditional options

Let’s be honest about what you’re giving up and what you’re gaining.

Traditional savings accounts currently offer around 0.5-1.5% APY in most countries. High-yield savings accounts might reach 4-5% APY.

DeFi stablecoin lending typically offers 3-10% APY on established platforms.

That’s 2-8 percentage points higher.

On a $10,000 deposit, here’s what that means:

- Traditional savings at 1% APY: $100 per year

- High-yield savings at 4% APY: $400 per year

- DeFi lending at 7% APY: $700 per year

The extra $300-600 annually comes with those risks we discussed: smart contract vulnerabilities, no insurance, regulatory uncertainty, and platform risks.

For some people, that trade-off makes sense. For others, it doesn’t.

Traditional finance vs DeFi: understanding the key differences helps you evaluate which system fits your risk tolerance.

Consider these factors:

- How much of your total savings are you considering for DeFi?

- Can you afford to lose this amount entirely?

- Do you have an emergency fund in traditional, accessible accounts?

- Are you comfortable with the technical complexity?

- Do you understand the tax implications in your jurisdiction?

If you’re putting your emergency fund or retirement savings into DeFi lending, you’re taking too much risk. This strategy works best for:

- Crypto-native funds you’re already comfortable holding

- Money you’ve allocated to higher-risk investments

- Amounts small enough that total loss wouldn’t affect your life

- Situations where you’re already holding stablecoins for other purposes

Advanced strategies once you’re comfortable with basics

After you’ve successfully deposited, earned interest, and withdrawn a few times, you might consider these approaches.

Yield farming across multiple platforms can optimize returns. Instead of keeping all funds in one protocol, you spread them across 2-3 platforms based on current rates. This requires more active management but reduces single-platform risk.

Using stablecoin lending as a hedge makes sense for some strategies. If you’re holding volatile crypto assets, keeping a portion in interest-bearing stablecoins provides stability while still earning returns.

Reinvesting interest automatically compounds your returns. Some platforms offer this feature, while others require manual reinvestment. On a 7% APY, reinvesting interest increases your effective annual return to about 7.25%.

Combining lending with borrowing creates leverage opportunities. You can deposit stablecoins, borrow against them at a lower rate, and deploy the borrowed funds elsewhere. This is advanced and risky but can amplify returns. How to borrow crypto without selling your assets explains the mechanics.

Monitoring rate changes actively lets you move funds when opportunities arise. Interest rates fluctuate based on market conditions. Moving funds to capture higher rates can boost returns, but gas fees might eat the gains on smaller amounts.

Participating in protocol governance sometimes offers additional rewards. Many platforms distribute governance tokens to lenders. Participating in votes and proposals can increase your token allocation.

These strategies require significantly more knowledge, time, and risk tolerance. Don’t attempt them until you’re completely comfortable with basic lending mechanics.

Watching for warning signs that something’s wrong

Knowing when to exit is just as important as knowing when to enter.

Several red flags should trigger immediate withdrawal:

Sudden APY spikes often indicate problems. If rates suddenly jump from 5% to 25%, it usually means something’s wrong with supply and demand. Either borrowers are desperate (bad sign) or the platform is offering unsustainable incentives (also bad).

Difficulty withdrawing is the biggest red flag. If your withdrawal takes longer than usual or fails repeatedly, get your funds out immediately. This often precedes platform failures.

Major token price drops in the protocol’s governance token can signal loss of confidence. While token prices fluctuate normally, sudden 50%+ drops often indicate serious issues.

Changes in team or leadership without clear communication deserve scrutiny. Anonymous team members suddenly leaving or major leadership changes can indicate internal problems.

Unusual smart contract activity visible on blockchain explorers might indicate an ongoing exploit. If you see large unexpected transactions, investigate immediately.

Regulatory announcements targeting your platform or stablecoin require attention. Don’t wait to see what happens. Withdraw first, assess later.

What happens when a DeFi protocol gets hacked explains what typically unfolds during security incidents.

Set up alerts for:

- Protocol Twitter accounts and Discord servers

- Blockchain security monitoring services

- Your wallet balance and transaction history

- Interest rate changes on your platform

Tax considerations you can’t ignore

This isn’t fun, but it’s necessary.

In most countries, interest earned on stablecoins counts as taxable income.

The IRS and equivalent agencies in other countries consider your DeFi interest as income in the year you receive it, even if you don’t withdraw it to fiat currency.

Here’s what you need to track:

- Date and amount of each deposit

- Interest accrued each day/month

- Date and amount of each withdrawal

- USD value of stablecoins at each transaction

- Gas fees paid (potentially deductible)

Some platforms provide transaction history exports, but many don’t. You’re responsible for tracking everything.

Consider using crypto tax software like CoinTracker or TokenTax if you’re earning significant interest. They can automatically import transactions and calculate tax obligations.

A few specific situations to understand:

Receiving governance tokens as rewards creates a taxable event at the moment you receive them, based on their market value.

Depositing stablecoins generally isn’t taxable (it’s like moving money between accounts).

Withdrawing stablecoins also isn’t taxable by itself.

The interest you earn is taxable as ordinary income.

Converting between stablecoins might trigger capital gains/losses if there’s a price difference.

Tax laws vary significantly by country and change frequently. This isn’t tax advice. Consult a tax professional familiar with cryptocurrency before filing.

Making your decision with realistic expectations

You now understand how earning interest on stablecoins actually works.

You know it’s legitimate, but not magic.

You know the yields come from real borrowers paying real interest.

You know the risks: smart contract bugs, stablecoin de-pegging, platform insolvency, regulatory changes, and user errors.

You know how to start small, test the process, and scale up carefully if it makes sense for your situation.

The question isn’t whether you can earn interest on stablecoins through DeFi lending. You absolutely can. Thousands of people do it successfully every day.

The question is whether you should, given your specific circumstances, risk tolerance, and financial goals.

If you’re comfortable with technology, understand the risks, can afford potential losses, and want exposure to DeFi yields, it’s worth trying with a small amount. Start with $100-500 on an established platform like Aave or Compound. Deposit, monitor, withdraw, and learn.

If the technical complexity feels overwhelming, if you can’t afford to lose the funds, or if the risks outweigh the extra 3-6% annual return for you, that’s completely reasonable. Traditional savings might offer lower yields, but they come with insurance, regulatory protection, and simplicity.

There’s no wrong answer. Just make sure you’re making an informed choice based on understanding, not hype.