Decentralized exchanges don’t use order books like traditional platforms. Instead, they rely on automated market makers that let you swap tokens instantly without waiting for a buyer or seller to match your order. This shift changes everything about how trading works, from pricing to liquidity.

Automated market makers use liquidity pools and mathematical formulas to enable instant token swaps on decentralized exchanges. Instead of matching buyers with sellers, AMMs let users trade against pooled assets while liquidity providers earn fees. This model makes decentralized trading possible but introduces unique risks like impermanent loss and slippage that don’t exist in traditional order book systems.

What automated market makers actually do

An automated market maker is a protocol that creates markets for any token pair without human market makers or order books.

You deposit tokens into a smart contract pool. The protocol uses a formula to determine prices. Anyone can trade against that pool instantly.

Traditional exchanges match your buy order with someone else’s sell order. AMMs eliminate that matching process entirely. The pool itself becomes your counterparty.

This matters because it solves the liquidity problem that plagued early decentralized exchanges. You don’t need thousands of active traders to create a functioning market. You just need enough tokens in the pool.

The breakthrough came when protocols like Uniswap proved this model could work at scale. Now most decentralized exchanges use some variation of the AMM model.

How liquidity pools replace order books

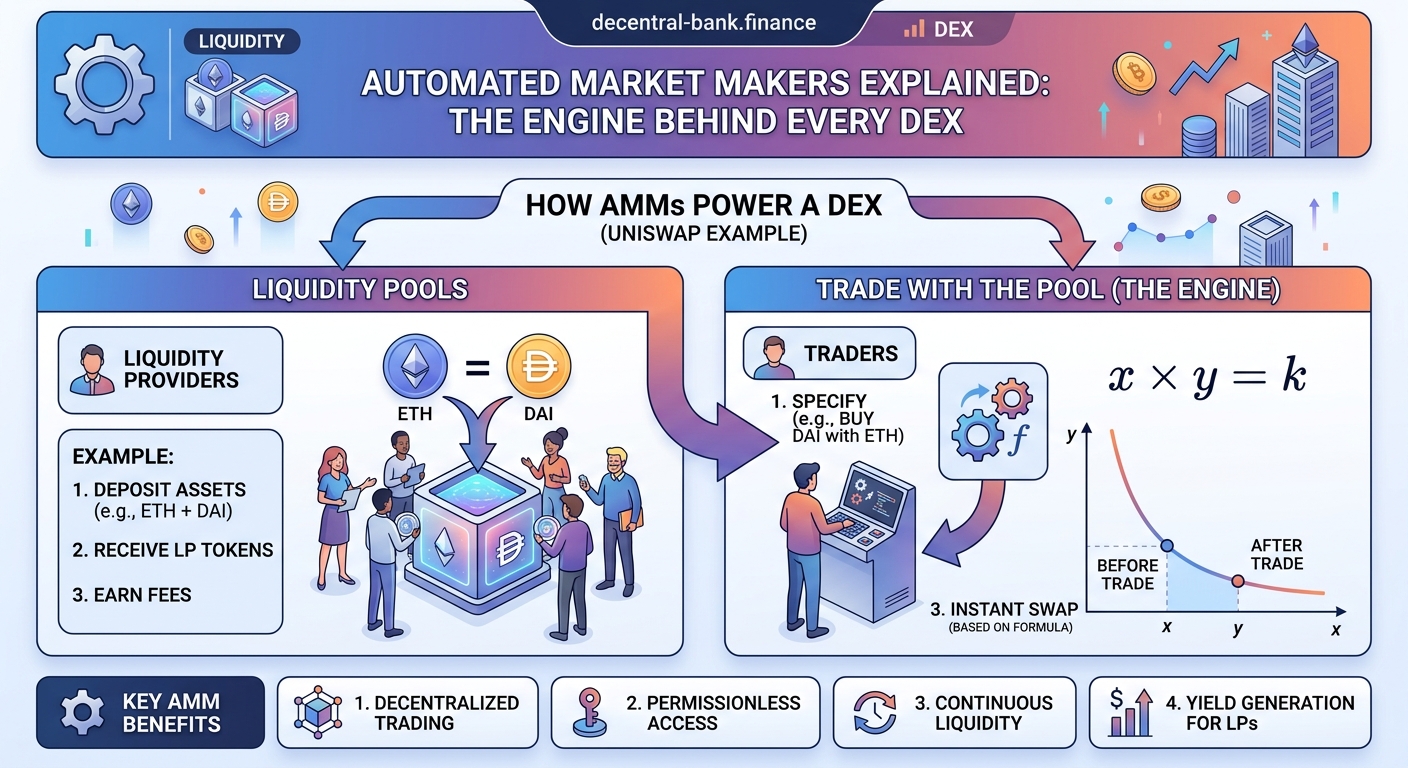

A liquidity pool is a smart contract holding two tokens in a specific ratio.

Let’s say you want to swap ETH for USDC. The pool might contain 100 ETH and 200,000 USDC. That 1:2000 ratio determines the current price.

When you trade, you add one token to the pool and remove the other. This changes the ratio, which changes the price for the next trader.

The pool maintains a constant relationship between the two token quantities. Most AMMs use the formula x * y = k, where x and y represent token quantities and k stays constant.

Here’s what happens during a swap:

- You send ETH to the pool

- The smart contract calculates how much USDC to give you based on the current ratio

- The pool’s new ratio reflects your trade

- The next trader sees a slightly different price

This mechanism works without any central authority managing prices or matching orders. The math handles everything.

Anyone can become a liquidity provider by depositing both tokens into a pool. In return, you earn a portion of trading fees. This creates incentives for people to supply the liquidity that makes trading possible.

Understanding how liquidity pools power most DeFi protocols helps you see why they’ve become the foundation of decentralized finance.

The constant product formula that powers most AMMs

The x * y = k formula is simpler than it looks.

If a pool has 100 ETH (x) and 200,000 USDC (y), then k equals 20,000,000. That number stays constant no matter how many trades happen.

When you buy 10 ETH from the pool, you’re removing ETH and adding USDC. The pool now has 90 ETH. To keep k constant at 20,000,000, it must have 222,222 USDC.

You just paid 22,222 USDC for 10 ETH. The average price was 2,222 USDC per ETH, higher than the starting price of 2,000 USDC per ETH.

This price impact increases with trade size. Small trades barely move the price. Large trades can shift it significantly.

The formula automatically adjusts prices based on supply and demand. When people buy ETH from the pool, ETH becomes scarcer and more expensive. When they sell ETH to the pool, it becomes more abundant and cheaper.

No human needs to set these prices. The math does it automatically, 24/7, across any token pair.

Different AMMs use variations of this formula. Curve uses a different equation optimized for stablecoins. Balancer allows pools with more than two tokens. But the core concept stays the same: algorithmic pricing based on pool ratios.

Why slippage happens on every AMM trade

Slippage is the difference between the price you expect and the price you actually get.

It happens because your trade changes the pool ratio before it completes. The bigger your trade relative to pool size, the worse your slippage.

Imagine swapping 50 ETH in that 100 ETH pool. You’re removing half the pool’s ETH supply. The formula has to dramatically increase the price to maintain the constant product.

Your effective price ends up much higher than the pool’s starting price. That difference is slippage.

Small pools have worse slippage than large pools. Trading $1,000 in a $10,000 pool moves the price significantly. Trading $1,000 in a $10,000,000 pool barely registers.

Most DEX interfaces show you estimated slippage before you confirm a trade. You can also set a maximum slippage tolerance. If actual slippage exceeds your limit, the transaction reverts.

Slippage can eat your profits if you’re not careful, especially when trading smaller tokens with limited liquidity.

Here’s a comparison of how trade size affects slippage:

| Trade Size (% of Pool) | Approximate Slippage | Impact on Your Trade |

|---|---|---|

| 1% | 0.1% | Minimal price difference |

| 5% | 0.5% | Noticeable but acceptable |

| 10% | 1.0% | Significant price impact |

| 25% | 3.5% | Major slippage, poor execution |

| 50% | 10%+ | Severe slippage, avoid if possible |

Professional traders split large orders into smaller chunks to minimize slippage. They might execute ten 1% trades instead of one 10% trade.

How liquidity providers make money and take risks

Liquidity providers deposit equal values of both tokens into a pool. In return, they receive LP tokens representing their share of the pool.

Every time someone trades, they pay a fee (usually 0.3% of trade value). That fee gets added to the pool, increasing its value. LP token holders earn a proportional share of all fees.

If a pool generates $10,000 in daily trading fees and you own 1% of the pool, you earn $100 per day. High-volume pools can generate substantial returns.

But there’s a catch called impermanent loss.

When token prices diverge from their original ratio, liquidity providers end up with more of the token that decreased in value and less of the token that increased in value.

Let’s say you deposit 1 ETH and 2,000 USDC when ETH costs $2,000. If ETH doubles to $4,000, arbitrage traders will buy cheap ETH from your pool until the ratio adjusts. You’ll end up with less ETH and more USDC than if you’d just held both tokens.

The loss is “impermanent” because it only becomes permanent if you withdraw your liquidity. If prices return to the original ratio, the loss disappears.

Understanding impermanent loss is critical before you start providing liquidity. Many beginners don’t realize this risk exists until they withdraw less value than they deposited.

Trading fees can offset impermanent loss, but only in high-volume pools. Low-volume pools might not generate enough fees to compensate for price divergence.

Before providing liquidity, calculate whether potential trading fees exceed potential impermanent loss. Use historical volatility and volume data to make informed decisions. Never provide liquidity to pools you don’t understand.

Different types of AMM models

The constant product formula (x * y = k) isn’t the only option. Different AMMs optimize for different use cases.

Constant product AMMs work best for volatile token pairs. Uniswap popularized this model. It handles any price range but creates significant slippage for large trades.

Stableswap AMMs use a different curve optimized for tokens that should trade near 1:1. Curve Finance pioneered this approach. It minimizes slippage for stablecoin swaps but breaks down if prices diverge too far.

Concentrated liquidity AMMs let providers specify price ranges where their liquidity is active. Uniswap v3 introduced this concept. It improves capital efficiency but requires active management.

Weighted pool AMMs allow pools with custom ratios, not just 50/50. Balancer lets you create pools with 80% of one token and 20% of another, or even pools with three or more tokens.

Each model makes different tradeoffs between simplicity, capital efficiency, and slippage. The right choice depends on what tokens you’re trading and how much liquidity exists.

For beginners, understanding how to compare order book versus AMM DEXs helps you pick the right platform for your needs.

How arbitrage keeps AMM prices accurate

AMMs don’t have price feeds or oracles telling them what tokens should cost. So how do prices stay accurate?

Arbitrage traders constantly monitor price differences between AMMs and other exchanges. When an AMM’s price drifts from the market rate, arbitrageurs profit by correcting it.

Here’s how it works:

- ETH trades at $2,000 on centralized exchanges

- An AMM pool’s ratio implies an ETH price of $1,950

- Arbitrageurs buy cheap ETH from the AMM

- They sell it for $2,000 on other exchanges

- This buying pressure pushes the AMM price back toward $2,000

This process happens automatically, often within seconds of a price discrepancy appearing. Arbitrage bots scan hundreds of pools constantly looking for profitable opportunities.

The larger and more liquid a pool, the smaller the arbitrage opportunities. Tiny price differences get corrected almost instantly in major pools. Smaller pools might drift further from accurate prices before arbitrageurs find it worthwhile to correct them.

Liquidity providers effectively subsidize this price accuracy. Arbitrageurs extract value from pools by buying low and selling high. That value comes from LPs who end up with less favorable token ratios.

This is another source of impermanent loss. Every arbitrage trade pushes LPs further from their original token balance.

Common mistakes that cost AMM users money

New users make predictable errors when using automated market makers.

Trading without checking slippage. You click swap, confirm the transaction, and get far fewer tokens than expected. Always review the estimated output and slippage percentage before confirming.

Providing liquidity to low-volume pools. You chase high APY numbers without checking actual trading volume. Fees never materialize, but impermanent loss does.

Ignoring gas fees. You try to swap $50 worth of tokens and pay $30 in gas fees. Small trades often don’t make economic sense on Ethereum mainnet.

Setting slippage too high. You set 5% slippage tolerance to ensure your trade goes through. MEV bots front-run your transaction and extract the maximum slippage you allowed.

Withdrawing liquidity during high volatility. Prices diverge significantly, you panic and withdraw, locking in maximum impermanent loss. Waiting for prices to revert would have reduced or eliminated the loss.

Here are the most common AMM mistakes and how to avoid them:

| Mistake | Why It Happens | How to Avoid It |

|---|---|---|

| Excessive slippage | Trading in small pools | Check liquidity depth before trading |

| Impermanent loss | Not understanding the mechanism | Calculate potential loss before providing liquidity |

| Failed transactions | Insufficient gas or slippage settings | Use recommended gas and realistic slippage |

| Front-running | High slippage tolerance | Set minimum acceptable slippage |

| Poor LP returns | Choosing pools by APY alone | Analyze volume, volatility, and fee generation |

Learning from common mistakes that could cost you crypto applies to AMM usage too. Many principles transfer across different DeFi activities.

Security considerations when using AMMs

AMMs eliminate counterparty risk from human market makers, but they introduce smart contract risk.

Every AMM runs on code. If that code has bugs, hackers can drain pools. Even audited contracts sometimes contain vulnerabilities that only become apparent after millions in TVL accumulate.

What happens when a DeFi protocol gets hacked shows the real consequences of smart contract failures.

Major AMMs like Uniswap have been battle-tested with billions in volume over years. Newer AMMs or forks might look identical but could contain subtle bugs or intentional backdoors.

Token approval exploits represent another risk. When you trade on an AMM, you must approve the contract to spend your tokens. Malicious contracts can request unlimited approval and drain your entire balance later.

Always check what you’re approving. Limit approvals to specific amounts when possible. Revoke old approvals periodically.

Understanding what happens when you approve a smart contract helps you avoid giving malicious contracts access to your funds.

Rug pulls are common in newer AMM pools. Developers create a token, provide initial liquidity, wait for others to buy in, then remove all liquidity and disappear with the funds.

Before trading or providing liquidity:

- Check if liquidity is locked

- Verify the token contract isn’t malicious

- Research the development team

- Look for audits from reputable firms

- Start with small amounts to test

Five free tools to check if a DeFi protocol is safe can help you evaluate AMMs before risking significant funds.

How AMMs connect to the broader DeFi ecosystem

Automated market makers don’t exist in isolation. They’re fundamental infrastructure that other DeFi protocols build on.

Lending platforms use AMM prices to determine collateral values. If you borrow against ETH, the protocol checks AMM pools to see what ETH is worth.

Yield farming strategies often involve providing liquidity to AMMs, then staking the LP tokens elsewhere for additional rewards. This creates layered yield opportunities.

Derivatives platforms reference AMM prices for settlement. Options and futures contracts might use Uniswap prices as their oracle.

Stablecoins depend on AMMs for maintaining their peg. When DAI trades above $1, arbitrageurs can mint new DAI and sell it on AMMs for profit, pushing the price back down.

This interconnection means AMM health affects the entire DeFi ecosystem. When AMM liquidity dries up, it impacts lending, derivatives, stablecoins, and more.

How DeFi actually works without banks or middlemen explains how these pieces fit together into a functioning financial system.

The composability of DeFi means you can build complex strategies using AMMs as building blocks. You might:

- Provide liquidity to earn fees

- Stake LP tokens to earn governance tokens

- Borrow against those governance tokens

- Use borrowed funds to provide more liquidity

Each step builds on the previous one, creating leverage and additional yield. It also compounds risk.

Calculating whether AMM trading makes sense for you

Not every trade belongs on an AMM. Sometimes centralized exchanges offer better execution.

Consider these factors:

Trade size relative to liquidity. If you’re trading more than 5% of pool depth, expect significant slippage. Centralized exchanges with deep order books might give better prices.

Gas fees versus trade value. On Ethereum, gas fees can exceed $20 during busy periods. Trading $100 worth of tokens means paying 20% in fees. That rarely makes sense.

Privacy preferences. AMMs don’t require KYC or accounts. If privacy matters more than optimal pricing, AMMs win despite higher costs.

Token availability. Many newer tokens only trade on AMMs. You can’t use centralized exchanges if the token isn’t listed there.

Custody preferences. AMMs let you trade directly from your wallet. You never give up custody. Centralized exchanges require depositing funds first.

For small trades of major tokens, centralized exchanges often provide better execution. For large trades, splitting across multiple venues might minimize overall slippage.

For newer tokens or privacy-focused users, AMMs remain the best option despite their limitations.

Understanding gas fees and how to minimize them helps you make smarter decisions about when AMM trading makes economic sense.

The future of automated market maker design

AMM technology continues to evolve rapidly. Current limitations are driving innovation in several directions.

Dynamic fees adjust based on volatility. When prices move quickly, fees increase to compensate liquidity providers for additional impermanent loss risk. Uniswap v3 experiments with this concept.

Just-in-time liquidity lets sophisticated LPs add liquidity right before large trades execute, earn the fees, then withdraw. This improves capital efficiency but might hurt passive LPs.

MEV mitigation tries to prevent bots from front-running trades and extracting value. Some AMMs now include MEV protection mechanisms that batch trades or hide transaction details.

Cross-chain AMMs enable swaps between tokens on different blockchains without bridges. This could eliminate bridge risk while expanding trading options.

Proactive market making uses oracles and off-chain data to adjust pool parameters before trades happen, reducing slippage and improving LP returns.

These innovations aim to reduce slippage, improve capital efficiency, and make liquidity provision more profitable. But they also add complexity.

Simpler AMM models remain easier to understand and audit. More complex designs might hide bugs or create new attack vectors.

The breakthrough DeFi innovations that could change how you manage crypto include several AMM improvements that might become mainstream soon.

Making AMMs work for your trading strategy

Automated market makers changed how decentralized trading works. They made it possible to swap any token without order books or centralized intermediaries.

The tradeoffs are real. Slippage, impermanent loss, and gas fees create costs that don’t exist on traditional exchanges. But the benefits of permissionless, non-custodial trading make those costs worthwhile for many users.

Start small when using AMMs. Test with amounts you can afford to lose while you learn how slippage and fees affect your trades. Compare prices across multiple AMMs before executing large swaps.

If you’re considering providing liquidity, understand impermanent loss thoroughly before depositing funds. Calculate whether fee income is likely to exceed potential losses based on historical volatility and volume.

The AMM model isn’t perfect, but it solved a fundamental problem that made early decentralized exchanges unusable. Now you can trade thousands of tokens instantly, any time, without permission. That’s the innovation automated market makers brought to DeFi.