Stablecoins promise the best of both worlds: the speed and accessibility of crypto with the predictable value of traditional money. But that promise only holds if the stability mechanisms actually work when markets turn volatile. Understanding whether stablecoins are safe requires looking beyond marketing claims to examine how reserves are managed, what regulatory oversight exists, and which technical vulnerabilities could put your funds at risk.

Stablecoins vary dramatically in safety depending on their backing mechanism, reserve transparency, regulatory compliance, and technical architecture. Fiat-backed stablecoins with audited reserves and clear redemption rights offer the highest safety, while algorithmic models carry significant depegging risk. Evaluating issuer credibility, custody arrangements, and smart contract security is essential before holding or transacting with any stablecoin.

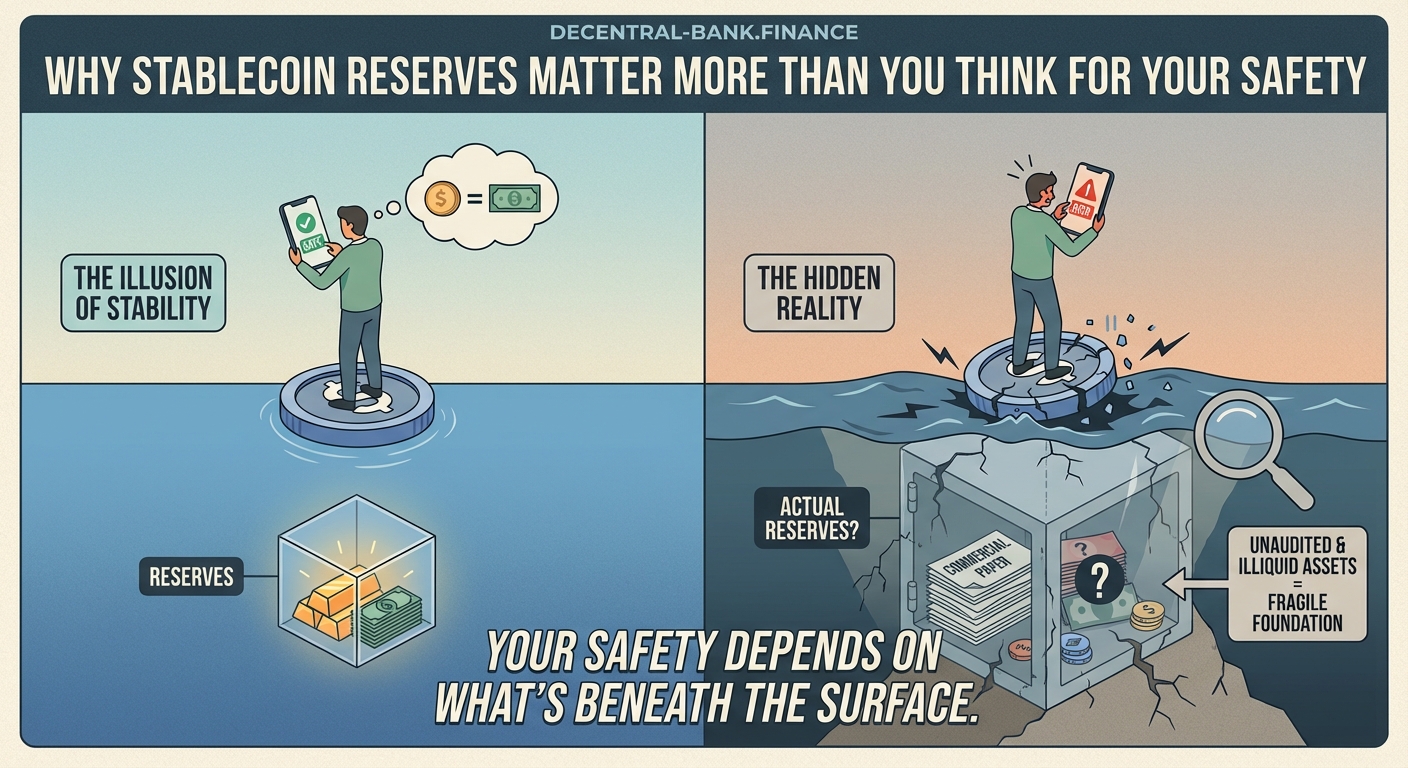

What makes a stablecoin safe or risky

Safety in stablecoins comes down to three core factors: the quality of backing assets, the transparency of reserve management, and the reliability of the peg mechanism.

Fiat-backed stablecoins hold traditional currency or equivalents in reserve. When managed properly, these offer straightforward value backing. Every token issued should correspond to a dollar, euro, or other asset held in custody. The risk emerges when reserves are incomplete, invested in risky instruments, or managed by entities without proper oversight.

Crypto-backed stablecoins use other digital assets as collateral, typically over-collateralized to absorb price volatility. A stablecoin might require $1.50 of Ethereum to back $1.00 of issued tokens. This buffer protects against price drops, but extreme market crashes can still trigger liquidations and depegging events.

Algorithmic stablecoins attempt to maintain their peg through supply adjustments and incentive mechanisms rather than asset backing. These models have repeatedly failed under stress, most notably with Terra’s UST collapse in 2022. The lack of tangible reserves makes them inherently more fragile during market panic.

Reserve composition matters enormously. A stablecoin backed entirely by cash and short-term Treasury bills carries minimal credit risk. One backed by commercial paper, corporate bonds, or crypto assets introduces counterparty risk and market volatility. The 2023 USDC depegging event, triggered by exposure to Silicon Valley Bank, demonstrated how even top-tier stablecoins face banking system risks.

How to evaluate stablecoin safety before using one

Assessing whether a specific stablecoin is safe requires systematic evaluation across multiple dimensions.

- Review the latest attestation or audit report from the issuer’s website, checking the date and scope of examination.

- Verify that reserves match or exceed the circulating supply, and identify what percentage consists of cash versus other instruments.

- Research the regulatory status of the issuer, including whether they operate under money transmitter licenses, e-money frameworks, or banking charters.

- Check the smart contract audit history and whether the code has been formally verified by reputable security firms.

- Assess the redemption process, including any restrictions, fees, minimum amounts, or verification requirements that could prevent you from converting back to fiat.

Transparency separates credible projects from questionable ones. Issuers publishing monthly attestations from recognized accounting firms demonstrate commitment to accountability. Those providing vague assurances or outdated reports raise red flags.

Regulatory compliance provides another safety layer. Stablecoins operating under clear legal frameworks in jurisdictions like the US, EU, or Singapore face oversight that reduces the likelihood of fraud or mismanagement. Unregulated issuers in opaque jurisdictions carry higher operational risk.

Smart contract security becomes critical for any stablecoin running on blockchain infrastructure. Even well-reserved stablecoins can be drained through code exploits, reentrancy attacks, or oracle manipulation. Multiple independent audits from firms specializing in blockchain security provide stronger assurance than a single review.

Understanding different risk profiles across stablecoin types

Not all stablecoins present the same risk profile, and understanding these differences helps match your use case with appropriate options.

| Stablecoin Type | Primary Risk | Transparency Level | Best Use Case |

|---|---|---|---|

| Fiat-backed (audited) | Banking system exposure | High with regular attestations | Business payments, large holdings |

| Fiat-backed (unaudited) | Reserve uncertainty | Low to medium | Short-term transactions only |

| Crypto-collateralized | Liquidation during volatility | High (on-chain verification) | DeFi applications |

| Algorithmic | Complete depegging | Medium (mechanism transparency) | Avoid for value storage |

Fiat-backed stablecoins with regular audits represent the safest category for most users. USDC and USDT dominate this space, though their risk profiles differ. USDC maintains higher transparency standards with monthly attestations and reserves held primarily in cash and short-term Treasuries. USDT offers broader exchange support and liquidity but has faced criticism over reserve disclosure practices.

Crypto-backed stablecoins like DAI provide unique advantages for users who want to avoid traditional banking system exposure. The over-collateralization model creates a buffer against volatility, and the collateral positions are verifiable on-chain. However, this model works best when underlying crypto assets maintain reasonable stability. During extreme market crashes, cascading liquidations can strain the system.

The safest stablecoin for your situation depends on your holding period, transaction size, and risk tolerance. For storing significant value long-term, prioritize fiat-backed options with strong regulatory compliance and transparent reserves. For interacting with DeFi protocols, crypto-backed alternatives may better align with your needs while keeping assets outside traditional finance.

Algorithmic stablecoins continue to attract developers seeking to create decentralized alternatives without reliance on custodians. The theoretical appeal is clear, but the practical track record shows repeated failures. Unless you’re actively trading with small amounts you can afford to lose, these models present unacceptable risk for serious financial use.

Security risks beyond the peg mechanism

Even stablecoins with solid backing face security challenges that can compromise user funds.

Smart contract vulnerabilities represent a persistent threat. Bugs in the code governing minting, burning, or transfers can be exploited by attackers. The 2023 Euler Finance hack, which affected DAI collateral, demonstrated how interconnected DeFi systems can create cascading risks even for well-designed stablecoins.

Custody arrangements determine who controls the reserve assets and under what conditions. Centralized stablecoins typically use regulated custodians with insurance and security protocols. Understanding whether reserves are segregated, how many signatories control access, and what happens in bankruptcy scenarios affects your safety.

Oracle manipulation poses risks for stablecoins that rely on external price feeds. If an attacker can temporarily distort the reported price of collateral assets, they might trigger inappropriate liquidations or mint tokens without proper backing. Robust oracle design using multiple data sources and time-weighted averages provides better protection.

Regulatory action creates another risk dimension. Authorities could freeze assets, force redemption restrictions, or shut down issuers deemed non-compliant. The 2023 enforcement actions against Binance and other crypto platforms highlighted how regulatory uncertainty affects even established stablecoins. Geographic diversification of reserves and legal structures can mitigate but not eliminate this risk.

Wallet security matters as much as stablecoin design. Holding stablecoins in exchange accounts exposes you to platform risk, as FTX users learned when that exchange collapsed. Choosing between hot wallets and cold wallets based on your transaction frequency and security needs provides better control over your assets.

What reserve transparency actually tells you

Reserve reports vary widely in quality and usefulness. Knowing how to interpret these disclosures helps you make informed safety assessments.

Attestations differ from audits. An attestation confirms that reserves matched liabilities at a specific point in time, but doesn’t verify the quality of those assets or examine internal controls. A full audit provides deeper assurance by reviewing processes, testing controls, and validating asset quality over a period.

Asset composition within reserves creates different risk profiles. Cash and Treasury bills offer maximum safety and liquidity. Commercial paper introduces credit risk from corporate issuers. Crypto assets add volatility. Some stablecoins hold a mix, and understanding the percentages helps gauge overall safety.

The attestation date matters more than many users realize. A report from six months ago tells you nothing about current reserves. Monthly or more frequent attestations demonstrate ongoing commitment to transparency. Real-time on-chain verification, available for some crypto-backed stablecoins, provides the highest confidence.

Redemption rights determine whether reserve backing translates into actual safety for you. Some stablecoins offer direct redemption only to large institutional users, forcing retail holders to rely on secondary market liquidity. Others provide universal redemption rights with clear processes. Understanding your actual ability to convert tokens back to fiat affects practical safety.

Common mistakes when evaluating stablecoin safety

Users frequently make assumptions that increase their risk exposure unnecessarily.

- Assuming all major stablecoins are equally safe without checking current reserve reports

- Confusing market capitalization or trading volume with safety or backing quality

- Ignoring the regulatory jurisdiction and legal protections available in case of issuer failure

- Holding stablecoins on centralized exchanges instead of in wallets where you control the keys

- Failing to diversify across multiple stablecoins when holding significant value

- Trusting algorithmic mechanisms without understanding the specific stability model and its failure modes

- Overlooking smart contract risks when using stablecoins in DeFi protocols

- Not monitoring for depegging events that might signal emerging problems

The assumption that “too big to fail” applies to stablecoins has been proven wrong multiple times. Even market leaders can face sudden crises. The March 2023 USDC depegging to $0.87 following Silicon Valley Bank’s collapse showed how quickly confidence can erode.

Regulatory clarity continues evolving. The 2024 Markets in Crypto-Assets (MiCA) regulation in Europe and ongoing US legislative efforts will reshape stablecoin oversight. How major DeFi protocols are responding to new regulatory frameworks offers context for understanding these changes.

Using stablecoins safely in practice

Implementing practical safety measures reduces your exposure to stablecoin risks.

For storing value, limit exposure to any single stablecoin. Diversifying across two or three well-reserved options reduces the impact if one experiences problems. Consider splitting holdings between USDC and USDT, or including a crypto-backed alternative like DAI for additional diversification.

For business payments, prioritize stablecoins with clear regulatory compliance and strong redemption infrastructure. The ability to convert large amounts back to fiat without delays or excessive fees matters more in commercial contexts than for personal use.

For DeFi participation, understand how your chosen protocols handle stablecoin collateral. Learning how to borrow crypto without selling your assets requires evaluating both the lending protocol’s safety and the stablecoin you’ll receive.

Monitor depegging events as early warning signals. Price deviations beyond 1-2% often indicate stress in the system. Having a plan to exit positions or convert to alternatives before a crisis fully develops protects your capital.

Verify you’re interacting with legitimate smart contracts. Phishing attacks often direct users to fake stablecoin contracts that steal deposits. Always check contract addresses against official sources before approving transactions.

The role of insurance and protection mechanisms

Some platforms and protocols offer additional safety layers beyond the stablecoin’s inherent design.

DeFi insurance protocols allow you to purchase coverage against smart contract failures, depegging events, or custodian hacks. While adding cost, this protection makes sense for larger holdings or extended time horizons. Coverage availability and claim processes vary significantly across providers.

Exchange insurance typically covers platform hacks but not stablecoin depegging or issuer insolvency. Understanding exactly what protection your exchange provides helps set appropriate expectations.

Some newer stablecoins incorporate insurance directly into their design, using a portion of revenue to fund protection pools. These mechanisms remain largely untested in major crisis scenarios.

Legal protections depend heavily on jurisdiction and issuer structure. Stablecoins issued by regulated banks may offer depositor protection up to certain limits. Those issued by non-bank entities typically provide no such guarantees, leaving holders as unsecured creditors in bankruptcy.

Comparing stablecoins to traditional alternatives

Understanding how stablecoin safety compares to conventional options provides useful context.

Bank deposits in developed countries typically carry government insurance up to $250,000 in the US or €100,000 in Europe. Stablecoins generally offer no equivalent protection, placing the entire risk on reserve quality and issuer reliability.

Money market funds invest in short-term debt instruments similar to some stablecoin reserves. They’re regulated investment vehicles with disclosure requirements, though they’re not risk-free. The 2008 financial crisis saw money market funds “break the buck,” falling below $1 per share.

Stablecoins offer advantages in speed, accessibility, and programmability that traditional alternatives can’t match. Cross-border payments that take days through banks settle in minutes with stablecoins. Integration with smart contracts enables automated payments and complex financial logic.

The tradeoff comes down to regulatory protection versus technological benefits. For amounts within insurance limits, bank deposits offer superior safety. For international transactions, DeFi integration, or amounts exceeding insurance caps, stablecoins may present acceptable risk given their unique capabilities.

Spotting warning signs before problems emerge

Certain indicators suggest increasing risk in a stablecoin before obvious failure occurs.

Declining transparency represents a major red flag. If an issuer stops publishing regular attestations, delays reports, or reduces disclosure detail, treat it as a warning signal. The pattern often precedes more serious problems.

Persistent small depegging events indicate stress in the stability mechanism. While brief deviations during volatile markets are normal, repeated or prolonged trading below peg suggests underlying issues.

Regulatory investigations or enforcement actions increase uncertainty and may restrict the issuer’s operations. Following news about your chosen stablecoins helps you stay ahead of developing situations.

Rapid growth in circulating supply without corresponding reserve increases suggests possible fractional backing. While issuers typically mint tokens only when receiving deposits, monitoring the relationship between supply growth and reported reserves can reveal discrepancies.

Changes in reserve composition toward riskier assets may indicate financial pressure. If a stablecoin shifts from primarily cash to commercial paper or other instruments, investigate whether this reflects deliberate strategy or necessity.

Making informed decisions about stablecoin use

The question of whether stablecoins are safe has no universal answer. Safety depends on which stablecoin you choose, how you use it, and what risks you’re willing to accept.

For short-term transactions and payments, well-established fiat-backed stablecoins with transparent reserves present minimal risk. The probability of a depegging event during a brief holding period is low, and the benefits of fast, low-cost transfers often outweigh the small risk.

For longer-term holdings, diversification across multiple stablecoins and careful monitoring become essential. No stablecoin has proven completely immune to problems, so concentration in a single option amplifies your exposure.

For DeFi participation, understanding both the stablecoin risks and the protocol risks you’re taking helps you make informed choices. Protecting yourself from DeFi rug pulls and exit scams extends beyond stablecoin selection to encompass the entire ecosystem.

Your risk tolerance, use case, and holding period should guide your stablecoin choices. Business treasuries face different constraints than individual traders. International payment needs differ from DeFi farming strategies. Matching stablecoin characteristics to your specific requirements produces better outcomes than following generic advice.

Building your stablecoin safety strategy

Creating a thoughtful approach to stablecoin use balances their benefits against their risks.

Start by identifying why you need stablecoins rather than traditional alternatives. If the answer is convenience rather than necessity, reconsider whether the additional risk makes sense. If stablecoins offer genuine advantages for your situation, proceed with appropriate safeguards.

Select stablecoins based on transparent criteria. Prioritize those with regular attestations, clear regulatory status, strong backing, and proven stability through previous market stress. Avoid newer or algorithmic models unless you have specific reasons and accept the higher risk.

Implement position limits that prevent catastrophic loss. Even with the safest stablecoins, holding your entire portfolio in these instruments concentrates risk unnecessarily. Determine appropriate allocation based on your overall financial situation.

Monitor your holdings regularly. Set up alerts for significant depegging events. Review reserve reports when published. Stay informed about regulatory developments affecting your chosen stablecoins.

Have an exit plan for different scenarios. Know how you’ll respond to minor depegging, major stability crises, or regulatory actions. Having predetermined thresholds and actions prevents emotional decision-making during stressful situations.

Your path to safer stablecoin use

Stablecoins offer powerful capabilities for anyone participating in crypto markets or needing efficient payment rails. Their safety ultimately depends on the quality of their design, the credibility of their issuers, and the care you take in selecting and managing them.

The transparency revolution in stablecoin reserves over recent years has made informed decision-making possible. You no longer need to trust vague promises. Attestations, audits, and regulatory frameworks provide concrete information for evaluating safety.

Your responsibility is using that information wisely. Check reserve reports before committing significant funds. Understand the specific risks of your chosen stablecoins. Implement practical safeguards like diversification and position limits. Stay alert to warning signs that might indicate emerging problems.

The stablecoins that survive and thrive will be those that prioritize safety through transparent reserves, regulatory compliance, and robust technical design. By choosing carefully and managing your exposure thoughtfully, you can benefit from stablecoin advantages while keeping your risk at acceptable levels.