Taking a collateralized crypto loan can feel like walking a tightrope. One wrong move and your assets get liquidated. The good news? You can calculate exactly where that danger zone begins before you borrow a single dollar. Understanding your liquidation price gives you control over your risk and helps you avoid painful surprises when markets turn volatile.

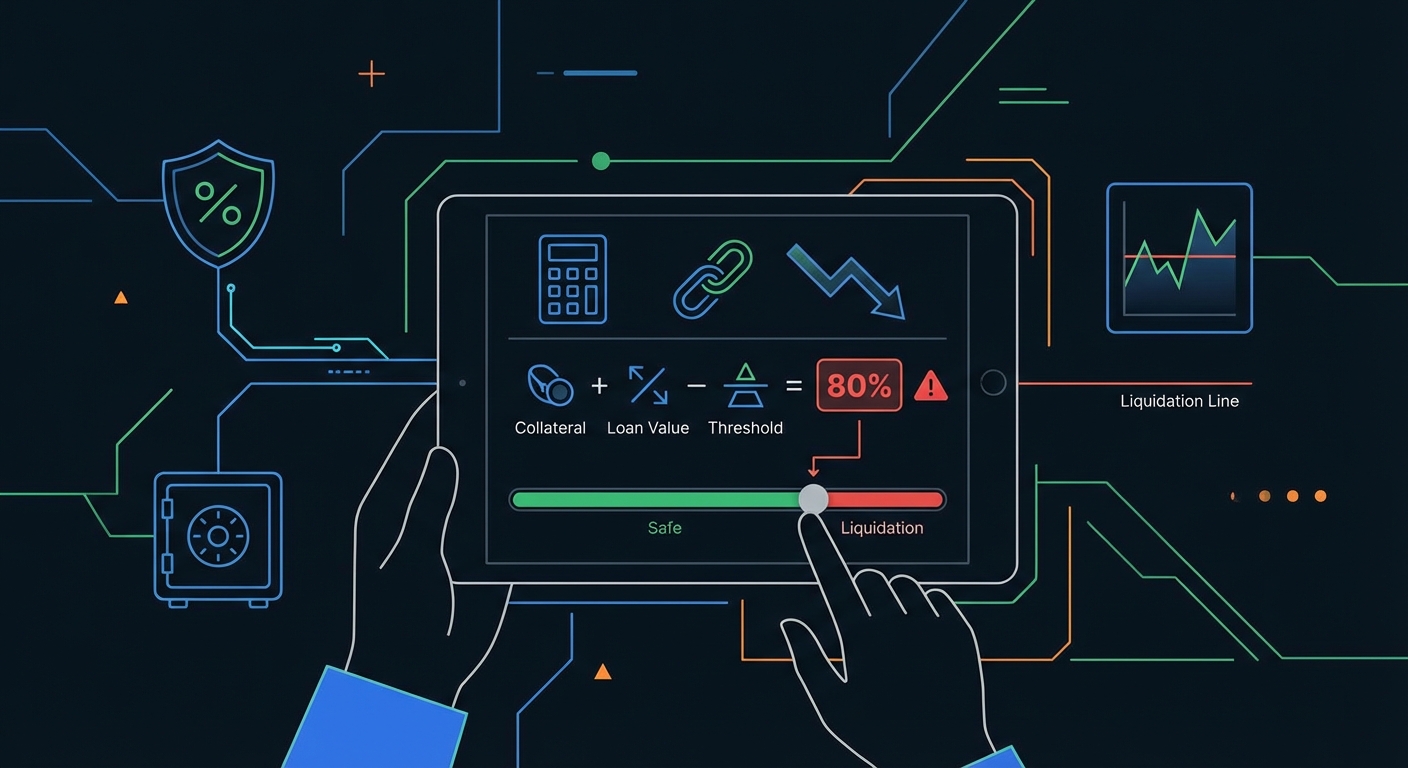

Calculating your liquidation price before taking a crypto loan helps you understand exactly when your collateral will be seized. The formula depends on your loan-to-value ratio, collateral amount, borrowed funds, and the protocol’s liquidation threshold. Knowing this number lets you manage risk, set price alerts, and add collateral before liquidation happens. Most DeFi protocols liquidate between 75% and 85% LTV ratios.

Understanding what liquidation actually means

Liquidation happens when your collateral value drops below a protocol’s safety threshold.

Imagine you deposit $10,000 worth of ETH and borrow $6,000 in stablecoins. If ETH’s price falls enough that your collateral no longer covers the loan plus a safety buffer, the protocol automatically sells your ETH to repay the debt.

This isn’t a punishment. It’s how how does DeFi actually work without banks or middlemen protocols protect lenders and maintain system stability.

The liquidation price is the exact collateral price point where this automatic sale triggers.

Different protocols use different thresholds. Aave might liquidate at 83% LTV. MakerDAO uses different ratios depending on collateral type. Compound has its own parameters.

Knowing your specific liquidation price helps you:

- Set price alerts before danger strikes

- Decide how much to borrow safely

- Plan when to add more collateral

- Avoid liquidation penalties and fees

The numbers you need before calculating

Before running any formula, gather these essential pieces of information.

Collateral amount: How much crypto you’re depositing (in USD value at current prices).

Loan amount: How much you’re borrowing (usually in stablecoins or other crypto).

Liquidation threshold: The maximum LTV ratio before liquidation. Find this in your protocol’s documentation. Most platforms display it clearly.

Current collateral price: The market price of your collateral asset right now.

Liquidation penalty: The fee charged when liquidation happens, typically 5% to 15%.

Let’s use a real example. You deposit 5 ETH when ETH trades at $2,000. That’s $10,000 in collateral. You borrow $6,000 USDC. Your protocol liquidates at 80% LTV.

Your loan-to-value ratio right now is $6,000 ÷ $10,000 = 60%.

You have breathing room before hitting that 80% threshold.

Step by step liquidation price formula

Here’s how to calculate where your collateral price needs to fall before liquidation triggers.

1. Identify your liquidation threshold percentage

Check your protocol’s documentation. Let’s say it’s 80% (or 0.80 in decimal form).

2. Calculate the critical collateral value

Divide your borrowed amount by the liquidation threshold:

Critical Collateral Value = Loan Amount ÷ Liquidation Threshold

Using our example: $6,000 ÷ 0.80 = $7,500

This means your total collateral value must stay above $7,500 to avoid liquidation.

3. Find the liquidation price per unit

Divide the critical collateral value by the number of units you deposited:

Liquidation Price = Critical Collateral Value ÷ Collateral Units

In our case: $7,500 ÷ 5 ETH = $1,500 per ETH

When ETH falls to $1,500, liquidation triggers.

4. Account for liquidation penalties

Most protocols charge a penalty when liquidating. This effectively raises your liquidation price slightly.

If the penalty is 10%, adjust your calculation:

Adjusted Critical Value = $7,500 × 1.10 = $8,250

Adjusted Liquidation Price = $8,250 ÷ 5 ETH = $1,650 per ETH

This gives you a more conservative safety margin.

Real world calculation examples

Let’s work through three common scenarios to cement your understanding.

Example 1: Bitcoin collateral on Aave

- Collateral: 0.5 BTC at $40,000 = $20,000

- Borrowed: $12,000 USDC

- Liquidation threshold: 75%

- Penalty: 5%

Critical value: $12,000 ÷ 0.75 = $16,000

With penalty: $16,000 × 1.05 = $16,800

Liquidation price: $16,800 ÷ 0.5 BTC = $33,600 per BTC

Example 2: Multiple collateral types

Things get trickier with mixed collateral. Each asset has its own liquidation threshold.

You deposit:

– 3 ETH at $2,000 = $6,000 (80% threshold)

– 0.2 BTC at $40,000 = $8,000 (75% threshold)

– Total collateral: $14,000

You borrow $8,000 USDC.

Calculate each asset’s weighted contribution:

ETH max loan: $6,000 × 0.80 = $4,800

BTC max loan: $8,000 × 0.75 = $6,000

Combined max: $10,800

Your current LTV: $8,000 ÷ $14,000 = 57%

This stays safe until your combined collateral value drops to: $8,000 ÷ 0.77 = $10,390 (weighted average threshold).

Example 3: Leveraged position

You deposit $5,000 ETH, borrow $3,000, buy more ETH, repeat.

After two loops you have:

– $11,000 total ETH collateral

– $6,000 total borrowed

– Current ETH price: $2,000

– Liquidation threshold: 80%

Critical value: $6,000 ÷ 0.80 = $7,500

You hold 5.5 ETH total.

Liquidation price: $7,500 ÷ 5.5 = $1,364 per ETH

Leverage magnifies both gains and liquidation risk.

Common mistakes that lead to unexpected liquidations

Even experienced DeFi users make calculation errors. Avoid these pitfalls.

| Mistake | Why it happens | How to avoid it |

|---|---|---|

| Ignoring liquidation penalties | Forgetting the 5-15% fee raises your effective liquidation price | Always multiply critical value by (1 + penalty rate) |

| Using entry price instead of current price | Collateral value changes constantly | Recalculate whenever prices move significantly |

| Forgetting about interest accumulation | Your debt grows over time with interest | Factor in annual percentage rate and loan duration |

| Assuming all protocols use the same threshold | Each platform sets different LTV limits | Check documentation for your specific protocol |

| Not accounting for price oracle delays | Oracle updates lag real market prices by seconds or minutes | Add a 2-5% safety buffer to your calculations |

| Mixing up LTV and liquidation threshold | LTV is current ratio, threshold is the limit | Liquidation threshold is always higher than safe LTV |

Interest accumulation deserves special attention. If you borrow $10,000 at 5% APR and hold the loan for one year, you actually owe $10,500. Your liquidation price calculation must use $10,500, not $10,000.

How different protocols handle liquidations

Each DeFi platform approaches liquidation differently. Understanding these nuances helps you calculate more accurately.

Aave uses a health factor system. When your health factor drops below 1.0, liquidation triggers. The formula is:

Health Factor = (Collateral × Liquidation Threshold) ÷ Borrowed Amount

A health factor of 1.5 means you’re 50% away from liquidation.

MakerDAO calls it a collateralization ratio. For ETH vaults, the minimum is typically 150%. Fall below that and you get liquidated.

Compound uses a borrow limit. You can borrow up to a percentage of your collateral value. Exceed it and face liquidation.

The math stays similar across platforms, but terminology changes.

When you’re learning how to borrow crypto without selling your assets, understanding these platform differences becomes critical.

Building a safety buffer into your calculations

Smart borrowers never get close to their liquidation price.

“I never borrow more than 50% of my maximum LTV. The 30% buffer has saved me from liquidation during every major crash since 2020. Sleep is worth more than extra yield.” – DeFi risk manager with $2M in active loans

Here’s how to build safety margins:

Strategy 1: Borrow at 50% of maximum LTV

If your protocol allows 75% LTV before liquidation, only borrow enough to reach 50% LTV. This gives you 25 percentage points of cushion.

Strategy 2: Set multiple price alerts

Create alerts at:

– 75% of distance to liquidation

– 85% of distance to liquidation

– 95% of distance to liquidation

Each alert gives you time to react.

Strategy 3: Keep extra collateral ready

Hold 20-30% additional collateral in how to choose between hot wallets and cold wallets for your crypto that you can deposit during crashes.

Strategy 4: Use stablecoins as partial collateral

Mixing volatile assets with how do stablecoins maintain their $1 peg during market crashes reduces overall portfolio volatility.

Tools and calculators that do the math for you

Manual calculation builds understanding, but automated tools save time and reduce errors.

Most DeFi protocols include built-in calculators showing your liquidation price in real time. Look for:

- Current health factor or LTV ratio

- Liquidation price display

- Simulation tools for different borrow amounts

- Price charts with liquidation markers

Third-party tools offer additional features:

DeFi Saver provides automated protection. Set your desired health factor and the tool automatically adds collateral or repays debt when needed.

Zerion shows portfolio-wide liquidation risks across multiple protocols in one dashboard.

DeBank tracks your positions and sends mobile notifications as you approach danger zones.

Instadapp offers one-click refinancing to move loans between protocols for better rates or higher LTV limits.

These tools complement your manual calculations. Verify their numbers match your own math, especially when large amounts are at stake.

What to do when you’re approaching liquidation

You’ve calculated your liquidation price. Now ETH is falling and you’re getting nervous. What are your options?

Option 1: Add more collateral

Deposit additional assets to increase your collateral value. This lowers your LTV ratio and pushes your liquidation price down.

If you deposited 5 ETH at $2,000 ($10,000) and borrowed $6,000, adding 2 more ETH increases collateral to $14,000 at current prices. Your LTV drops from 60% to 43%.

Option 2: Repay part of the loan

Reducing your debt decreases the LTV ratio. Repaying $2,000 of that $6,000 loan brings your LTV from 60% to 40%.

You don’t need to repay everything. Even partial repayment buys breathing room.

Option 3: Swap to less volatile collateral

Some protocols let you swap collateral types without closing your position. Moving from ETH to a wrapped BTC or stablecoin LP token might reduce volatility.

Option 4: Close the position entirely

Sometimes the safest move is exiting. Repay the full loan, withdraw your collateral, and wait for calmer markets.

Option 5: Refinance to a different protocol

If another platform offers higher LTV limits or lower liquidation thresholds, you might move your loan there. This requires careful execution to avoid getting liquidated during the transfer.

Managing multiple loans across protocols

Many DeFi users maintain positions on several platforms simultaneously. Tracking liquidation prices becomes more complex.

Create a spreadsheet with these columns:

- Protocol name

- Collateral asset and amount

- Current collateral price

- Borrowed asset and amount

- Liquidation threshold

- Calculated liquidation price

- Current LTV ratio

- Health factor or distance to liquidation

Update this weekly, or daily during volatile markets.

Consider correlation between your collateral assets. If you have ETH collateral on Aave and also on Compound, both positions face similar risk during an ETH crash. Diversifying collateral types spreads risk.

Some users deliberately spread loans across protocols to avoid putting all eggs in one basket. Smart contract risk, oracle failures, and governance changes affect different platforms differently.

Understanding how to protect yourself from DeFi rug pulls and exit scams becomes essential when managing multiple positions.

Advanced considerations for experienced borrowers

Once you master basic liquidation calculations, these advanced factors matter.

Oracle price manipulation: Your liquidation price depends on the oracle price, not necessarily the market price. During extreme volatility or low liquidity, these can diverge. Chainlink, Band Protocol, and other oracles update at different speeds.

Flash crash protection: Some protocols implement time-weighted average prices or require multiple oracle confirmations. This prevents single-block price manipulation but can also delay liquidations.

Partial liquidations: Many modern protocols only liquidate enough collateral to bring you back to a safe LTV ratio, not your entire position. Calculate what percentage gets liquidated at different price points.

Liquidation cascades: During market crashes, mass liquidations can trigger more liquidations. Your calculated liquidation price might execute at a worse price due to slippage if thousands of positions liquidate simultaneously.

Gas price spikes: Adding collateral during emergencies costs gas. On Ethereum, gas can spike to 500+ gwei during volatility. Keep ETH for gas in your wallet.

Cross-margin vs isolated margin: Some protocols pool all your collateral (cross-margin) while others keep each loan separate (isolated). Cross-margin offers better capital efficiency but creates interconnected liquidation risk.

Regulatory and tax implications of liquidations

Getting liquidated isn’t just financially painful. It creates tax reporting complexity.

In most jurisdictions, liquidation counts as a taxable event. You’ve effectively sold your collateral at the liquidation price. If that price exceeds your cost basis, you owe capital gains tax.

If ETH cost you $1,000 but liquidated at $1,500, you have a $500 taxable gain per ETH, even though you lost money overall on the loan.

Keep detailed records:

– Original collateral deposit date and price

– Loan origination date and amount

– Liquidation date and price

– Fees paid

– Any partial repayments or collateral additions

Some users in the U.S. have successfully argued that liquidation creates a capital loss rather than a gain if the total position lost money. Consult a crypto-specialized tax professional.

The regulatory landscape keeps evolving. How major DeFi protocols are responding to new regulatory frameworks in 2024 affects how platforms handle liquidations and reporting.

Testing your calculation skills

Let’s practice with a challenging scenario.

You hold a leveraged position:

– Deposited 10 ETH when ETH was $1,800 = $18,000 initial

– Borrowed $10,000 USDC, bought 5.55 more ETH

– Total collateral now: 15.55 ETH

– Current ETH price: $2,000

– Total collateral value: $31,100

– Liquidation threshold: 82%

– Liquidation penalty: 8%

What’s your liquidation price?

Step 1: Critical collateral value = $10,000 ÷ 0.82 = $12,195

Step 2: Adjust for penalty = $12,195 × 1.08 = $13,171

Step 3: Liquidation price = $13,171 ÷ 15.55 ETH = $847 per ETH

Your current LTV is $10,000 ÷ $31,100 = 32%. You have substantial room before liquidation.

But notice how leverage affects the calculation. Your liquidation price ($847) sits far below your average entry price (roughly $1,800). The borrowed funds let you buy more ETH, which provides a bigger cushion.

However, if ETH rises to $2,500, your collateral becomes worth $38,875, but you still owe only $10,000. Your LTV drops to 26%. The liquidation price also rises to $1,059 per ETH because you’re calculating based on more total value.

Leverage creates asymmetric risk and reward.

Why knowing your numbers changes everything

Calculating your liquidation price transforms borrowing from gambling into informed risk management.

You stop worrying about every 5% price swing. You know exactly where danger begins. You can set alerts, plan responses, and sleep better.

Most liquidations happen to borrowers who either never calculated their threshold or forgot to monitor it during volatility. Don’t be that person.

Take 10 minutes before every loan to run the numbers. Write them down. Set calendar reminders to recalculate weekly. Update your spreadsheet when you adjust positions.

The formula isn’t complicated. The discipline to use it consistently makes all the difference.

Your crypto deserves better than panic-checking prices at 3 AM wondering if you’re about to get liquidated. Calculate once, monitor regularly, and borrow with confidence.