Watching your collateral disappear in a liquidation event feels terrible. One moment you’re borrowing against your crypto, the next moment the protocol has sold your assets and closed your position. The worst part? Most liquidations are completely preventable.

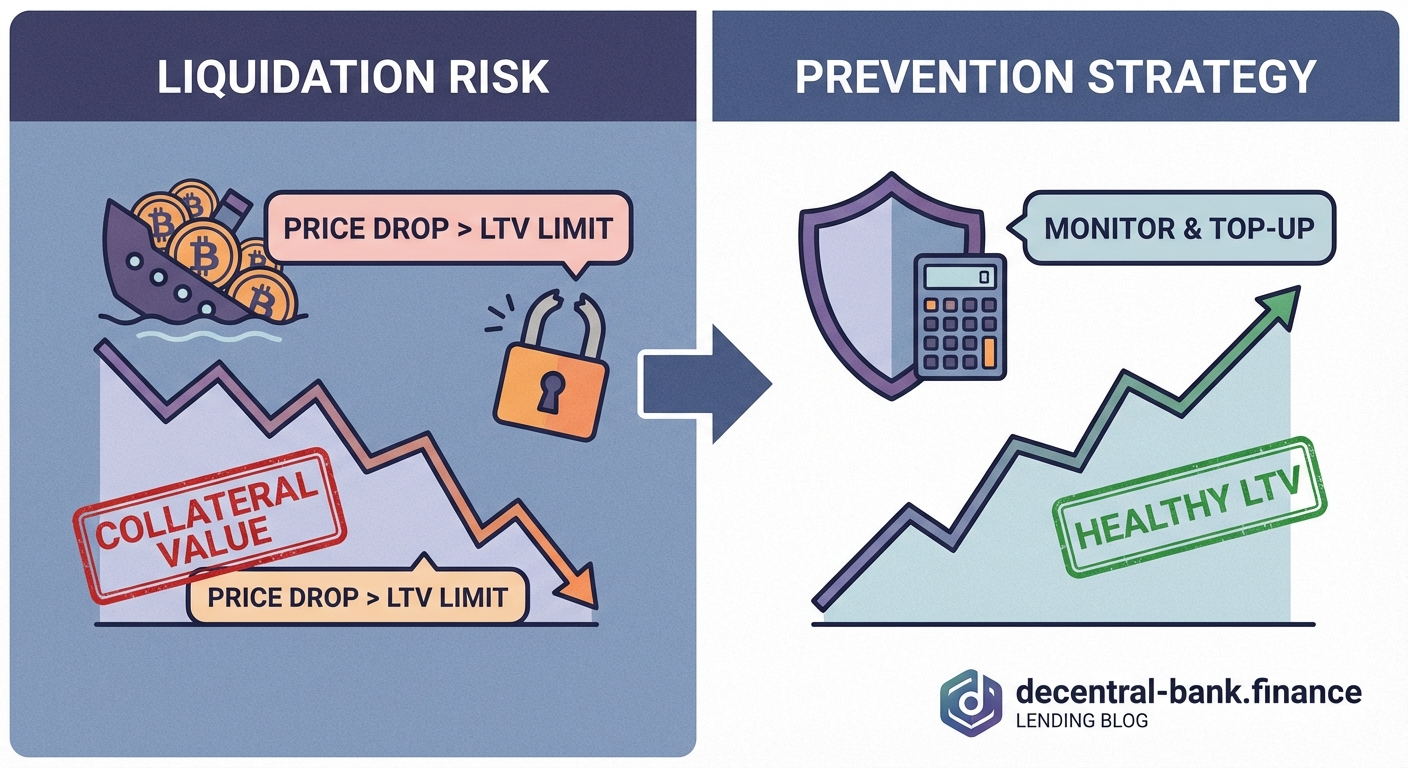

Crypto loan liquidations happen when your collateral value drops below required thresholds. You can prevent them by maintaining conservative loan-to-value ratios, monitoring health factors daily, keeping emergency reserves, setting up alerts, and responding immediately to margin calls. Understanding these mechanics protects your positions during market volatility.

Understanding why liquidations actually happen

Liquidation isn’t punishment. It’s a safety mechanism.

When you borrow crypto without selling your assets, you lock up collateral. The protocol needs to ensure your collateral always covers your loan plus interest. If your collateral value drops too far, the protocol automatically sells it to repay lenders.

Think of it like a margin call in traditional finance, except there’s no phone call. The smart contract executes automatically.

Most protocols use a loan-to-value (LTV) ratio to measure risk. If you deposit $10,000 in ETH and the maximum LTV is 75%, you can borrow up to $7,500. But here’s the catch: that ratio changes every second as crypto prices move.

When ETH drops 20%, your $10,000 collateral becomes $8,000. Your $7,500 loan hasn’t changed, so your LTV jumps from 75% to 93.75%. You’re now in the danger zone.

Different protocols set different thresholds:

- Maximum LTV: The highest ratio allowed when opening a loan

- Liquidation threshold: The ratio that triggers automatic liquidation

- Liquidation penalty: Extra fees charged when you get liquidated

The gap between maximum LTV and liquidation threshold is your safety buffer. Smaller gaps mean less room for error.

The five steps that prevent liquidation

Following these steps in order gives you the best protection against losing your collateral.

1. Never borrow at maximum capacity

The biggest mistake is maxing out your borrowing power.

If a protocol allows 75% LTV, borrow at 50% instead. This gives you a 25 percentage point cushion before you approach danger. That cushion can absorb a 33% price drop in your collateral before you need to worry.

Calculate your personal maximum like this:

Take the liquidation threshold and multiply by 0.65. If liquidation happens at 80% LTV, your personal maximum should be 52% (80% × 0.65 = 52%).

This conservative approach means you’re leaving borrowing power on the table. That’s the point. You’re trading potential profit for actual safety.

2. Monitor your health factor every single day

Most DeFi protocols display a “health factor” or “health ratio” on your dashboard. This number tells you how close you are to liquidation.

A health factor of 2.0 means your collateral is worth twice your liquidation threshold. A health factor of 1.0 means you’re about to be liquidated. Below 1.0, liquidation has already started.

Check this number daily. Set a calendar reminder. Make it part of your morning routine like checking email.

When your health factor drops below 1.5, take action immediately. Don’t wait to see if the market recovers. It might not.

3. Keep emergency reserves ready to deploy

You need ammunition to defend your position when markets turn ugly.

Set aside 20-30% of your collateral value in stablecoins. Keep these funds in a hot wallet you can access instantly, not locked in staking or liquidity pools.

When your health factor drops, you have two options:

- Add more collateral to increase your cushion

- Repay part of your loan to lower your LTV

Both actions improve your health factor. Having reserves ready means you can act within minutes, not hours or days.

Some people keep these reserves on the same protocol where they’re borrowing. This allows instant deposits without waiting for transfers. Just remember that funds sitting on a protocol carry smart contract risk.

4. Set up automated alerts and actually respond to them

Every major lending protocol offers notification systems. Turn them all on.

Configure alerts for these thresholds:

- Health factor drops below 2.0 (early warning)

- Health factor drops below 1.5 (urgent action needed)

- Health factor drops below 1.2 (emergency)

Connect alerts to multiple channels: email, SMS, Telegram, Discord. Redundancy matters because you might miss one notification but not all of them.

When an alert fires, stop what you’re doing and check your position. Markets move fast. A health factor of 1.3 can become 1.0 in minutes during extreme volatility.

“The difference between keeping your collateral and losing it often comes down to response time. Set up alerts you’ll actually notice, and treat them like smoke alarms, not suggestions.” – DeFi Risk Management Best Practices

5. Understand liquidation cascades and how to avoid them

Liquidation cascades happen when one liquidation triggers price drops that cause more liquidations. These cascades are most common during market crashes.

Here’s how they unfold:

When a large position gets liquidated, the protocol dumps collateral on the market. This selling pressure pushes prices lower. Lower prices trigger more liquidations. More liquidations create more selling pressure. The cycle feeds itself.

You can’t prevent cascades, but you can avoid getting caught in them. Watch for these warning signs:

- Funding rates on perpetual contracts hitting extremes

- Open interest reaching all-time highs

- Social media filled with leverage bragging

- Multiple protocols showing elevated liquidation risks

When you see these signals, reduce your LTV even further. Better to miss some upside than lose your collateral.

Comparing prevention strategies

Different approaches work for different risk tolerances. Here’s how the main strategies stack up:

| Strategy | Protection Level | Capital Efficiency | Best For |

|---|---|---|---|

| 50% maximum LTV | High | Low | Conservative holders |

| Daily monitoring + reserves | Medium-High | Medium | Active managers |

| Automated rebalancing | High | High | Technical users |

| Stablecoin collateral only | Very High | Very Low | Risk-averse borrowers |

| Multiple smaller positions | Medium | Medium | Diversification focused |

The right strategy depends on how much time you can dedicate to management and how much risk you’re comfortable taking.

Conservative holders should use low LTV ratios and check positions weekly. Active managers can push LTV higher but must monitor daily and maintain larger reserves. Technical users can set up automated systems that add collateral or repay loans when thresholds are breached.

Common mistakes that lead to liquidation

Learning from others’ errors is cheaper than making your own.

Borrowing against volatile altcoins: Using small-cap tokens as collateral is extremely risky. A 50% drop can happen in hours. Stick to major assets like BTC and ETH for collateral.

Ignoring margin call warnings: Protocols give you advance notice. If you ignore a health factor of 1.3 hoping for a recovery, you’re gambling with your collateral.

Keeping all reserves locked up: Staking rewards and LP fees are great until you need liquidity immediately. Always keep some funds available for emergencies.

Using multiple protocols without tracking total exposure: Borrowing from Aave, Compound, and MakerDAO simultaneously makes it harder to track your overall risk. Consolidate positions when possible.

Forgetting about accruing interest: Your loan balance grows daily from interest. Even if prices stay flat, your LTV ratio slowly increases. Factor interest into your calculations.

Trusting oracle updates will always be timely: During extreme volatility, price oracles can lag reality. Your actual risk might be higher than what the dashboard shows.

What happens during an actual liquidation

Understanding the mechanics helps you appreciate why prevention matters.

When your position crosses the liquidation threshold, the protocol opens your loan for liquidation. In most systems, third-party liquidators (often bots) compete to close your position.

The liquidator repays your loan and receives your collateral plus a liquidation bonus. This bonus typically ranges from 5% to 15% of the collateral value. That bonus comes directly from your pocket.

Let’s walk through a real example:

You deposit $10,000 in ETH and borrow $7,000 in stablecoins at 70% LTV. ETH drops 30%, so your collateral is now worth $7,000. Your LTV ratio is now 100%. Liquidation triggers.

A liquidator repays your $7,000 loan and receives $7,700 worth of your ETH (including a 10% liquidation penalty). You’re left with $300 worth of ETH, minus any additional protocol fees.

You started with $10,000. You end with roughly $300. The $7,000 you borrowed is gone (presumably spent or deployed elsewhere). You’ve lost 97% of your collateral.

This is why prevention is everything.

Advanced protection techniques

Once you’ve mastered the basics, these techniques add extra layers of safety.

Partial position management: Instead of one large loan, split your collateral into multiple smaller positions. If one gets liquidated, you only lose part of your collateral. This approach requires more gas fees but provides better risk isolation.

Collar strategies with options: Buy put options on your collateral to protect against downside. If ETH drops, your put gains value and you can use those gains to add collateral. This insurance costs money but can save your position.

Automated debt ceiling systems: Some advanced users set up smart contracts that automatically repay portions of loans when health factors drop. This requires technical knowledge but provides 24/7 protection.

Cross-collateral diversification: Use multiple types of collateral in the same loan. If one asset crashes, the others might hold steady. Protocols like Aave support this approach.

Yield farming your reserves: Keep your emergency reserves in low-risk yield strategies like stablecoin pools that allow instant withdrawal. You earn some return while maintaining liquidity.

Platform-specific considerations

Different protocols have different liquidation mechanics. Understanding these differences helps you choose safer platforms.

Aave uses a health factor system and allows you to switch between stable and variable interest rates. Their liquidation threshold is typically higher than their maximum LTV, giving you a buffer.

Compound liquidates up to 50% of your debt at once. This can be harsh but prevents total position loss. Their liquidation discount is around 8%.

MakerDAO charges a liquidation penalty of 13% and requires you to manage your collateralization ratio manually. They offer more control but less hand-holding.

Centralized platforms like BlockFi or Celsius (before its collapse) handled liquidations differently. They often had opaque processes and less predictable thresholds. This is one reason many users prefer transparent DeFi protocols.

Read the documentation for any platform before depositing collateral. Know exactly when liquidation triggers and what penalties apply.

Building your personal safety checklist

Create a written checklist you follow every time you open or manage a loan position.

Before opening a position:

- Calculate maximum safe LTV (liquidation threshold × 0.65)

- Verify you have 25-30% reserves available

- Set up monitoring alerts

- Confirm you understand the liquidation penalty

- Check current market volatility levels

During active management:

- Review health factor daily

- Check collateral price trends weekly

- Verify alerts are working monthly

- Reassess your LTV ratio after major market moves

- Keep notes on why you opened the position (helps prevent emotional decisions)

When receiving alerts:

- Check health factor immediately

- Calculate how much collateral or repayment needed

- Execute the transaction within 30 minutes

- Verify the action improved your health factor

- Document what triggered the alert for future reference

Having a written process removes emotion from decision-making. When your health factor is 1.15 and dropping, you don’t want to be figuring out what to do. You want to execute a pre-planned response.

Recovery strategies if you’re already near liquidation

Sometimes you inherit a bad position or miss warning signs. Here’s how to respond when you’re in immediate danger.

Triage assessment: Check your health factor right now. If it’s below 1.2, you’re in emergency mode. Stop reading and add collateral or repay debt immediately.

If you’re between 1.2 and 1.5, you have a bit more time but not much. Calculate exactly how much additional collateral you need to reach a health factor of 2.0. Then add 20% more than that calculation.

Finding emergency funds: If you don’t have reserves ready, you need to source funds fast. Options include:

- Withdrawing from other DeFi positions (accept the gas costs)

- Selling other crypto holdings (accept the tax implications)

- Borrowing from a friend or partner (accept the social awkwardness)

- Using a credit card to buy stablecoins (expensive but sometimes necessary)

None of these options are ideal. That’s why maintaining reserves is so important.

Partial position closure: If you can’t source enough funds to save the entire position, consider voluntarily closing part of it. Repay enough debt to get your health factor above 2.0, even if it means realizing a loss.

A controlled partial closure is better than a full liquidation. You keep more of your collateral and avoid the liquidation penalty.

Protecting yourself from protocol-specific risks

Platform risk is separate from market risk but equally important.

Smart contract bugs can cause unexpected liquidations. DeFi protocols occasionally have vulnerabilities that malicious actors exploit. While major platforms like Aave and Compound are heavily audited, risk never reaches zero.

Diversify across protocols if you’re borrowing large amounts. Don’t put all your collateral in one platform, no matter how reputable.

Oracle failures can trigger false liquidations. If a price oracle reports incorrect data, the protocol might think your position is underwater when it’s actually safe. This is rare but has happened.

Governance changes can alter liquidation parameters. DAOs sometimes vote to change LTV ratios, liquidation thresholds, or penalties. Follow governance forums for protocols where you have active positions.

Network congestion can prevent you from adding collateral during emergencies. During the May 2021 crash, Ethereum gas fees exceeded $500 per transaction. Some users couldn’t afford to save their positions. This is another argument for maintaining higher safety buffers.

The psychology of managing leveraged positions

Technical knowledge isn’t enough. You need emotional discipline.

Greed makes you borrow too much: When crypto is pumping, borrowing at 75% LTV feels safe. You’re leaving money on the table by being conservative. This thinking gets people liquidated.

Fear makes you close positions too early: After getting burned once, some people become overly cautious. They maintain 30% LTV and miss opportunities. Balance is key.

Hope makes you ignore warnings: “The market will bounce back” is dangerous thinking when your health factor is 1.3. Hope is not a strategy.

Panic makes you make mistakes: Seeing a 1.15 health factor triggers adrenaline. You might send funds to the wrong address or approve a malicious contract. Have procedures in place before emergencies happen.

Successful leverage users treat positions like a business, not a casino. They follow rules even when it feels unnecessary. They close positions when targets are hit. They don’t let emotions override their systems.

Building long-term sustainable borrowing habits

The goal isn’t to avoid liquidation once. It’s to borrow safely for years.

Start small. Your first loan should be tiny, even if you can afford much more. Learn the interface. Practice adding collateral. Get comfortable with the monitoring tools. Make mistakes when they’re cheap.

Track every position in a spreadsheet. Record the opening date, initial LTV, collateral type, borrowed amount, health factor, and any actions taken. Review this log monthly. You’ll start seeing patterns in your behavior.

Calculate your total cost of borrowing. Interest rates are obvious, but also factor in gas fees, monitoring time, and the opportunity cost of keeping reserves liquid. Sometimes borrowing isn’t worth it.

Set position size limits based on your total portfolio. A common rule is never borrow more than 20% of your total crypto holdings. This ensures one bad position can’t wipe you out.

Review and adjust your strategy quarterly. What worked in a bull market might not work in a bear market. Your risk tolerance might change as your portfolio grows. Stay flexible.

When borrowing might not be the right choice

Sometimes the best way to avoid liquidation is not borrowing at all.

If you can’t check your positions daily, don’t open leveraged loans. The risk is too high. Consider staking instead for passive income without liquidation risk.

If you need the borrowed funds for expenses you can’t afford to lose, don’t borrow against crypto. Use crypto as collateral only when you can afford to lose it.

If you’re borrowing to buy more crypto (leverage), understand you’re amplifying both gains and losses. Most retail traders lose money with leverage over time.

If the protocol is new or unaudited, don’t risk your collateral. Stick to established platforms with long track records.

If you don’t understand how the liquidation process works, don’t borrow until you do. Read the documentation. Test with small amounts. Knowledge prevents expensive mistakes.

Your collateral deserves better protection

Liquidation is a solved problem. The tools exist to prevent it. The strategies are proven. The difference between success and failure comes down to discipline.

Start with conservative LTV ratios. Monitor your positions daily. Keep emergency reserves ready. Set up alerts and respond immediately. These aren’t suggestions, they’re requirements for safe borrowing.

Your crypto has value because you chose not to sell it. Don’t let a preventable liquidation make that choice for you. Take the time to implement proper risk management today, and you’ll never see that sickening “position liquidated” notification.

The market will test you. Volatility will come. Your preparation today determines whether you weather the storm or lose your collateral. Choose preparation.