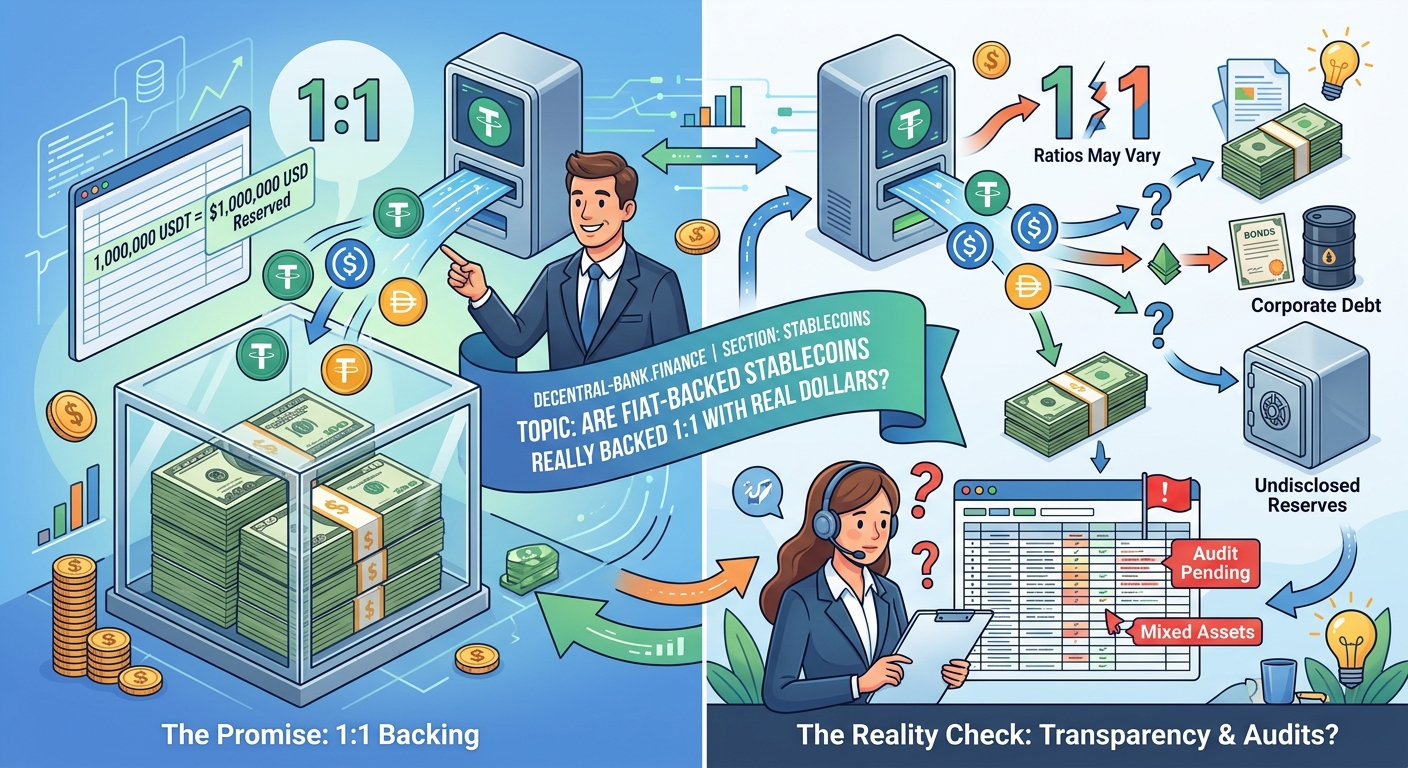

You’ve probably heard the promise a hundred times: one stablecoin equals one dollar, always redeemable, always safe. But when you actually look at how these digital assets maintain their value, the picture gets a lot more complicated. Some stablecoins hold actual cash in bank accounts. Others hold Treasury bills, commercial paper, or a mix of assets that might not be as liquid as you’d hope. And a few? They don’t hold traditional reserves at all.

Fiat-backed stablecoins claim 1:1 dollar backing, but reserves vary widely. Some hold cash and short-term Treasuries. Others use commercial paper or mixed assets. Transparency differs dramatically between issuers. Understanding what actually backs your stablecoin determines whether you can redeem it during market stress. Always verify reserve composition and audit frequency before trusting any stablecoin with significant funds.

What “backed by real dollars” actually means

When stablecoin issuers say they’re backed by real dollars, they’re making a specific claim. For every token in circulation, they supposedly hold one dollar’s worth of assets in reserve.

But “dollar’s worth” does a lot of heavy lifting in that sentence.

Some issuers hold actual U.S. dollars in bank accounts. Others hold short-term Treasury bills that mature in weeks or months. Some hold commercial paper issued by corporations. A few hold a blend of cash, bonds, and other instruments that theoretically add up to the right value.

The difference matters enormously when you try to redeem your tokens.

Cash sitting in a bank account? Available immediately. Treasury bills maturing in three months? You might need to sell them at a discount if everyone rushes for the exits at once. Commercial paper from a struggling company? That could lose value fast during a financial crisis.

Here’s what different reserve types actually mean for you:

| Reserve Type | Liquidity | Risk Level | Redemption Speed |

|---|---|---|---|

| Cash deposits | Immediate | Low | Same day |

| Short-term Treasuries | High | Very low | 1-3 days |

| Commercial paper | Medium | Moderate | 3-7 days |

| Mixed assets | Varies | Higher | Uncertain |

| Crypto collateral | Variable | High | Depends on market |

How major stablecoins structure their reserves

Let’s look at how the biggest players actually back their tokens.

USDC publishes monthly attestation reports from a major accounting firm. These reports show the exact composition of their reserves. As of recent reports, USDC holds primarily cash and short-term U.S. Treasury bonds. Circle, the issuer, allows qualified institutions to redeem tokens directly for dollars.

USDT takes a different approach. Tether publishes quarterly reports showing a mix of assets. These include cash, Treasury bills, commercial paper, secured loans, and other investments. The exact breakdown changes over time. Critics point out that Tether’s reserves have historically included riskier assets than pure cash equivalents.

DAI operates on an entirely different model. This decentralized stablecoin backs itself with cryptocurrency collateral locked in smart contracts. You can see exactly what backs DAI at any moment by checking the blockchain. The system requires over-collateralization, meaning $150 worth of crypto might back $100 worth of DAI. When collateral values drop too far, the system automatically liquidates positions to maintain backing.

BUSD was backed by Paxos with a reserve structure similar to USDC. It held cash and cash equivalents in FDIC-insured U.S. banks and published monthly attestation reports. However, Paxos stopped issuing new BUSD tokens in 2023 following regulatory pressure.

Understanding these differences helps you choose which stablecoin matches your risk tolerance. If you’re getting started with DeFi, knowing reserve structures protects you from nasty surprises.

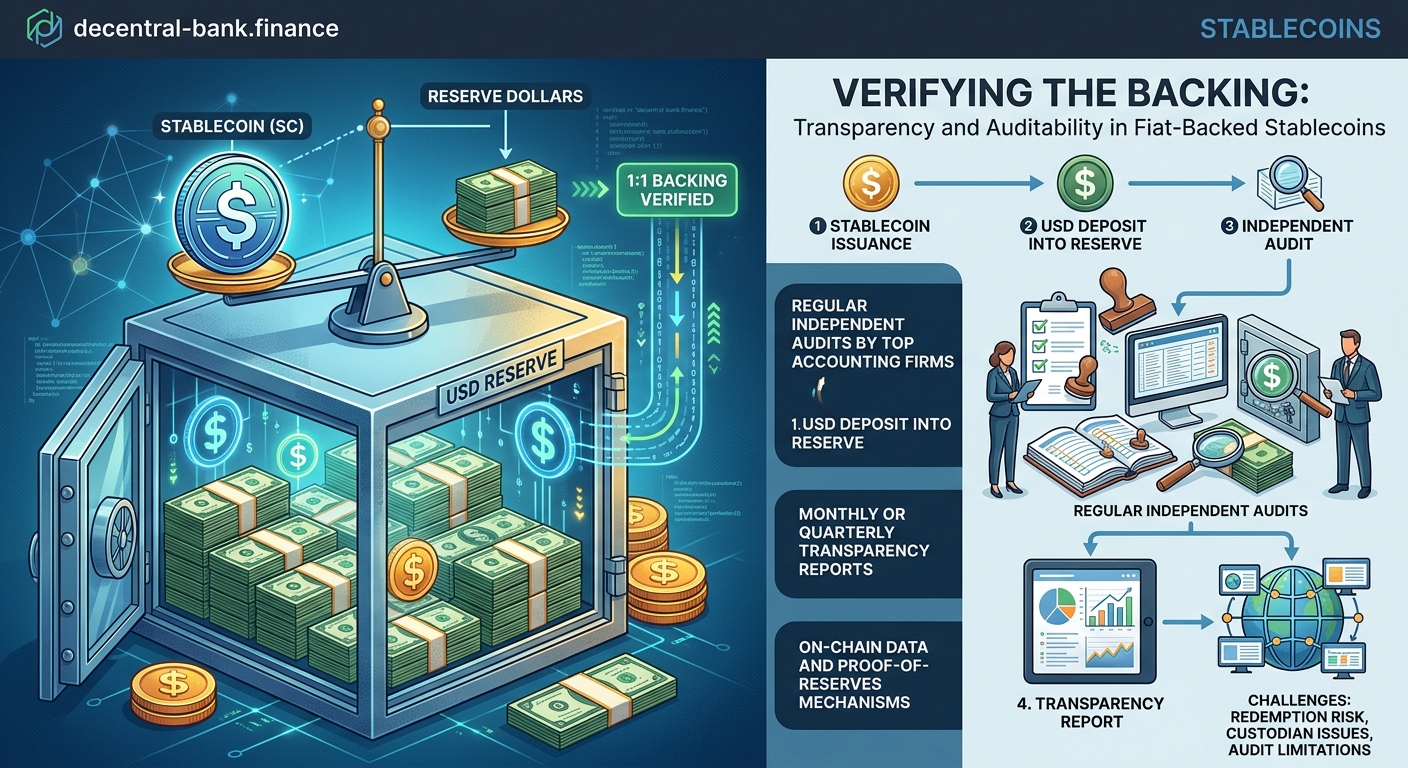

The transparency problem

Here’s where things get frustrating for users trying to verify backing claims.

Most stablecoin issuers don’t provide real-time proof of reserves. Instead, they publish periodic reports. These reports might come monthly, quarterly, or even less frequently. The delay matters because reserve composition can change significantly between reports.

Attestation reports also differ from full audits. An attestation verifies that reserves matched liabilities at a specific moment in time. It doesn’t examine the quality of those reserves, the issuer’s operational controls, or whether the same assets might be pledged multiple times.

Some issuers have faced criticism for the opacity of their reserve holdings. Questions about asset quality, bank relationships, and redemption mechanisms persist across the industry.

The best way to evaluate a stablecoin’s backing is to read the actual attestation reports yourself. Don’t rely on marketing claims. Look at the numbers, check the asset breakdown, and verify the attestation firm’s credentials.

A few stablecoins have started providing more granular transparency. Some publish daily updates. Others use blockchain-based proof of reserves that anyone can verify. These innovations help, but they’re not yet industry standard.

The lack of standardized reporting makes comparing stablecoins difficult. One issuer might classify an asset as “cash equivalent” while another puts the same asset in a different category. Without consistent definitions, users struggle to make informed choices.

Can you actually redeem stablecoins for dollars?

This is where theory meets reality.

Most stablecoin issuers restrict direct redemption to specific users. You typically need to be a verified institutional customer, meet minimum redemption amounts (often $100,000 or more), and go through KYC procedures.

Regular retail users don’t redeem stablecoins directly with issuers. Instead, they sell tokens on exchanges or through decentralized exchanges for other cryptocurrencies or fiat currency.

This creates a crucial distinction: the stablecoin might be backed 1:1, but you personally might not be able to access that backing directly.

Here’s how redemption typically works for different user types:

-

Institutional users contact the issuer directly, verify their identity, and request redemption. The issuer transfers dollars to their bank account and burns the corresponding tokens.

-

Retail users sell stablecoins on an exchange. The price they receive depends on market supply and demand, not just the reserve backing.

-

DeFi users swap stablecoins through automated market makers. Slippage and liquidity conditions affect the actual value received.

During periods of market stress, these redemption mechanisms can break down. If everyone tries to sell stablecoins simultaneously, exchange liquidity dries up. Prices can temporarily fall below $1 even if reserves remain fully backed.

The 2022 collapse of UST demonstrated this risk dramatically. Despite algorithmic mechanisms designed to maintain the peg, the token lost nearly all its value when redemption pressure overwhelmed the system. While UST wasn’t backed by traditional reserves, the event highlighted how redemption mechanisms matter as much as backing.

What happens during a bank run

Stablecoins face the same fundamental challenge as traditional banks. If everyone tries to withdraw at once, even fully backed reserves might not prevent problems.

Consider a stablecoin backed by three-month Treasury bills. These are extremely safe assets. But if you need to sell billions of dollars worth in a single day, you might have to accept prices below face value. That gap between the reserve value and the redemption value creates risk.

Some stablecoins address this by holding a larger percentage of reserves in immediately liquid cash. Others maintain credit facilities that provide emergency liquidity. A few have implemented circuit breakers that slow redemptions during stress periods.

None of these solutions is perfect. Higher cash reserves mean lower returns for the issuer. Credit facilities depend on counterparties remaining willing to lend during crises. Circuit breakers might prevent panic but also reduce confidence in redemption guarantees.

The fundamental tension remains: maintaining a stable $1 value requires both adequate reserves and the ability to convert those reserves to cash quickly. Understanding how stablecoins maintain their peg helps you evaluate whether specific tokens can withstand stress.

Red flags that suggest insufficient backing

Certain warning signs should make you question a stablecoin’s reserve claims.

Lack of regular attestations tops the list. If an issuer doesn’t publish monthly or quarterly reports from a reputable accounting firm, you have no way to verify their backing claims. Marketing promises mean nothing without independent verification.

Vague reserve descriptions raise concerns. Phrases like “backed by a basket of assets” or “fully collateralized” without specific breakdowns hide important information. You need to know exactly what assets back the tokens.

Frequent changes in reserve composition suggest instability. While some variation is normal, dramatic shifts between reports might indicate the issuer is struggling to maintain backing or taking excessive risks with reserves.

Restrictions on redemptions beyond normal institutional requirements are problematic. If an issuer imposes unexpected limits, delays, or conditions on redemptions, it might signal reserve problems.

Regulatory issues provide another warning. Stablecoins facing enforcement actions, regulatory investigations, or banking relationship problems might struggle to maintain backing or process redemptions.

History of de-pegging events deserves scrutiny. A stablecoin that has temporarily lost its $1 peg multiple times might have structural problems with its reserve management or redemption mechanisms. Learning what happens when stablecoins lose their peg prepares you for these scenarios.

Comparing fiat-backed versus crypto-backed models

The two main approaches to stablecoin backing offer different trade-offs.

Fiat-backed stablecoins hold traditional financial assets. They depend on banks, custody relationships, and traditional financial infrastructure. This creates regulatory risk but also provides familiarity and potentially stronger legal protections.

Crypto-backed stablecoins use digital assets as collateral. Everything happens on-chain where anyone can verify it. You don’t need to trust attestation reports because you can check the reserves yourself. But you accept the volatility risk of the underlying crypto collateral.

Fiat-backed stablecoins typically offer:

- Lower technical complexity

- Easier regulatory compliance

- Direct dollar backing

- Dependence on banking relationships

- Centralized control

- Opaque reserve management

Crypto-backed stablecoins provide:

- Full transparency

- Decentralized verification

- No bank dependencies

- Higher collateral requirements

- Smart contract risks

- Volatility exposure

Neither model is inherently superior. Your choice depends on which risks you prefer to accept. If you want maximum transparency and don’t mind over-collateralization, crypto-backed stablecoins like DAI make sense. If you prioritize simplicity and regulatory compliance, fiat-backed options might suit you better.

For those interested in the technical differences, exploring crypto-collateralized versus fiat-backed stablecoins reveals additional nuances.

What regulators are demanding

Regulatory scrutiny of stablecoins has intensified significantly.

Regulators increasingly demand that stablecoin issuers meet standards similar to banks or money market funds. This includes capital requirements, reserve restrictions, and regular examinations.

Some jurisdictions now require stablecoins to hold reserves only in cash and short-term government securities. Commercial paper, corporate bonds, and other assets face restrictions or outright bans.

Redemption rights are another regulatory focus. Authorities want clear, enforceable rights for users to redeem tokens for dollars. The current system where only institutions can redeem directly doesn’t satisfy regulatory expectations for retail protection.

Segregation of reserves from operating capital is becoming mandatory. Issuers can’t use reserve assets for business operations, investments, or lending. The money backing tokens must remain separate and available.

Insurance requirements are under discussion. Some proposals would require stablecoins to carry insurance protecting users against reserve losses or operational failures.

These regulatory changes will likely reshape the stablecoin landscape. Issuers unable or unwilling to meet new standards might exit the market. Those that comply might gain competitive advantages through enhanced credibility.

Understanding how major DeFi protocols respond to regulatory frameworks shows how the industry is adapting.

Practical steps to verify backing

You can’t blindly trust stablecoin marketing. Here’s how to do your own verification.

-

Find the latest attestation report. Visit the issuer’s website and locate their reserve reports. These should be published regularly by a recognized accounting firm.

-

Check the report date. Older reports might not reflect current conditions. Monthly reports are better than quarterly. Real-time verification is best.

-

Examine the asset breakdown. Look at what percentage sits in cash versus other instruments. Higher cash percentages generally mean better liquidity.

-

Verify the accounting firm. Make sure a legitimate, established firm conducted the attestation. Unknown or questionable firms raise red flags.

-

Compare tokens in circulation to reserve value. The reserves should equal or exceed the total token supply. Any shortfall is a major warning sign.

-

Review redemption terms. Understand who can redeem, under what conditions, and what minimums apply. This affects whether the backing matters for you personally.

-

Check for recent de-pegging events. Look at price history on major exchanges. Frequent or severe deviations from $1 suggest problems.

-

Research regulatory status. Determine whether the issuer faces investigations, enforcement actions, or banking difficulties.

For those using stablecoins in DeFi, knowing essential things to check before buying any stablecoin prevents costly mistakes.

When backing guarantees break down

Even fully backed stablecoins can fail under certain conditions.

Operational failures represent one risk. If the issuer loses access to banking relationships, they might be unable to process redemptions even with adequate reserves. Several stablecoins have faced this problem when banks suddenly terminated relationships.

Fraud or mismanagement can drain reserves. If executives misappropriate funds or make unauthorized investments, the backing disappears regardless of what attestation reports claimed previously.

Legal seizures might freeze reserves. Government actions, bankruptcy proceedings, or court orders could prevent the issuer from accessing reserves to honor redemptions.

Smart contract bugs affect crypto-backed stablecoins. Even if collateral exists, programming errors might prevent proper liquidations or allow unauthorized minting.

Market manipulation can temporarily break pegs. Large coordinated selling, even of a fully backed stablecoin, might push prices below $1 until arbitrageurs restore balance.

Contagion from related failures creates risk. If a stablecoin issuer has business relationships with failing companies, panic might spread even if direct backing remains intact.

These scenarios explain why backing alone doesn’t guarantee safety. Operational competence, legal structure, and market confidence all matter too. Understanding the real risks of stablecoin de-pegging prepares you for these possibilities.

Making informed choices about stablecoins

Your stablecoin choice should match your specific use case and risk tolerance.

For short-term transactions and trading, backing matters less than liquidity and exchange support. The most widely accepted stablecoins often work best even if their reserve transparency isn’t perfect.

For longer-term holdings or significant amounts, reserve quality becomes critical. You want stablecoins with strong attestations, conservative reserve policies, and proven redemption mechanisms.

For DeFi applications, consider whether you need compatibility with specific protocols. Some DeFi platforms work better with certain stablecoins. Technical integration might outweigh minor differences in backing.

For regulatory compliance, choose stablecoins from issuers meeting jurisdictional requirements. This matters especially if you’re a business or dealing with large amounts.

For privacy considerations, understand that most major stablecoins have KYC requirements and can freeze addresses. If privacy matters, you might need to accept trade-offs in backing transparency or regulatory compliance.

Diversification across multiple stablecoins reduces concentration risk. Don’t put all your funds in a single stablecoin, regardless of how well-backed it claims to be.

Regular monitoring of your chosen stablecoins protects you. Reserve compositions change. Regulatory situations evolve. Market conditions shift. What was safe six months ago might be riskier today.

If you’re exploring broader DeFi opportunities, learning about earning interest on stablecoins through DeFi lending shows how to put your stablecoins to work.

Understanding the future of stablecoin backing

The stablecoin market is evolving rapidly toward greater transparency and stricter standards.

More issuers are adopting real-time proof of reserves using blockchain technology. This allows anyone to verify backing continuously rather than waiting for periodic reports.

Regulatory frameworks are converging on requirements similar to narrow banks or money market funds. Expect stricter rules about reserve composition, segregation, and redemption rights.

Decentralized alternatives are improving. Crypto-backed stablecoins are becoming more capital-efficient while maintaining transparency. Algorithmic models are learning from past failures and implementing better stability mechanisms.

Traditional financial institutions are entering the market. Banks and payment companies launching stablecoins might bring stronger regulatory compliance but also more centralized control.

Central bank digital currencies will compete with private stablecoins. Government-issued digital dollars might offer ultimate backing security but sacrifice the permissionless access that makes current stablecoins useful for DeFi without banks or middlemen.

The question isn’t whether stablecoins are backed by real dollars. It’s whether the specific stablecoin you’re using has the right kind of backing for your needs, whether you can actually access that backing when needed, and whether the issuer can maintain backing during market stress.

Your next steps with stablecoins

Now you understand that “backed by real dollars” means different things for different stablecoins.

Start by reviewing the reserve reports for any stablecoins you currently hold. Verify that backing matches your assumptions. If you discover concerning information, consider switching to alternatives with better transparency.

For new stablecoin purchases, make verification part of your routine. Don’t buy based on marketing claims alone. Check the latest attestation, examine the reserve breakdown, and understand the redemption process.

Remember that backing is necessary but not sufficient for safety. Operational competence, regulatory compliance, and market confidence all contribute to whether a stablecoin maintains its peg.

Stay informed about regulatory developments affecting stablecoins. Changes in rules might make some options more or less attractive over time.

Consider your actual redemption options realistically. If you can’t redeem directly with the issuer, the theoretical backing matters less than market liquidity and exchange support.

The stablecoin market will continue evolving. Better transparency, stronger regulations, and improved technology will make backing verification easier. But the fundamental responsibility remains yours: understand what backs your stablecoins before trusting them with your money.