You see a DeFi protocol offering 15% APY on stablecoins and wonder if it’s too good to be true.

Traditional banks pay less than 1% on savings accounts. Credit unions might stretch to 2% if you’re lucky. Meanwhile, DeFi protocols advertise double-digit returns like it’s nothing.

The gap feels suspicious. You’re right to be skeptical.

Understanding why DeFi yields are so high requires looking at what these protocols actually do with your money, who pays for those returns, and what could go wrong. The answer isn’t a scam, but it’s not risk-free either.

DeFi yields are high because protocols eliminate middlemen, pass savings to users, and compensate for real risks like smart contract vulnerabilities, impermanent loss, and liquidation. Returns come from lending fees, trading commissions, and token incentives, not magic. Higher yields always signal higher risk, and understanding the source of your APY is essential before depositing funds into any protocol.

Where DeFi yields actually come from

Banks make money by lending your deposits at higher rates than they pay you.

They keep the difference as profit. That spread covers their buildings, employees, compliance teams, and shareholders.

DeFi protocols cut out these costs entirely.

When you deposit funds into a lending protocol like Aave or Compound, you’re directly lending to borrowers. The protocol charges borrowers interest and passes most of it to you, minus a small protocol fee.

No branch managers. No marble lobbies. No quarterly earnings calls.

The efficiency creates higher base rates. But that’s just the start.

Trading fees drive liquidity pool returns

Decentralized exchanges like Uniswap don’t hold inventory. They rely on users to deposit token pairs into liquidity pools.

When someone swaps ETH for USDC, they pay a small fee. That fee gets distributed to everyone who provided liquidity to that pool.

High trading volume means high fees. Popular pairs can generate substantial returns from trading activity alone.

The catch? You’re exposed to impermanent loss, which can eat into or exceed your trading fee earnings if token prices move significantly.

Token incentives boost APY artificially

Many protocols offer governance tokens as additional rewards.

They’re trying to attract users and build liquidity. These token rewards can push APY into triple digits, especially for new protocols.

But here’s the reality check: those tokens have no guaranteed value.

If the protocol fails or the token price crashes, your “200% APY” becomes worthless. You might lose more than you gained, especially if you had to buy and deposit tokens at their peak price.

Early users often profit. Late arrivals get stuck holding depreciating tokens.

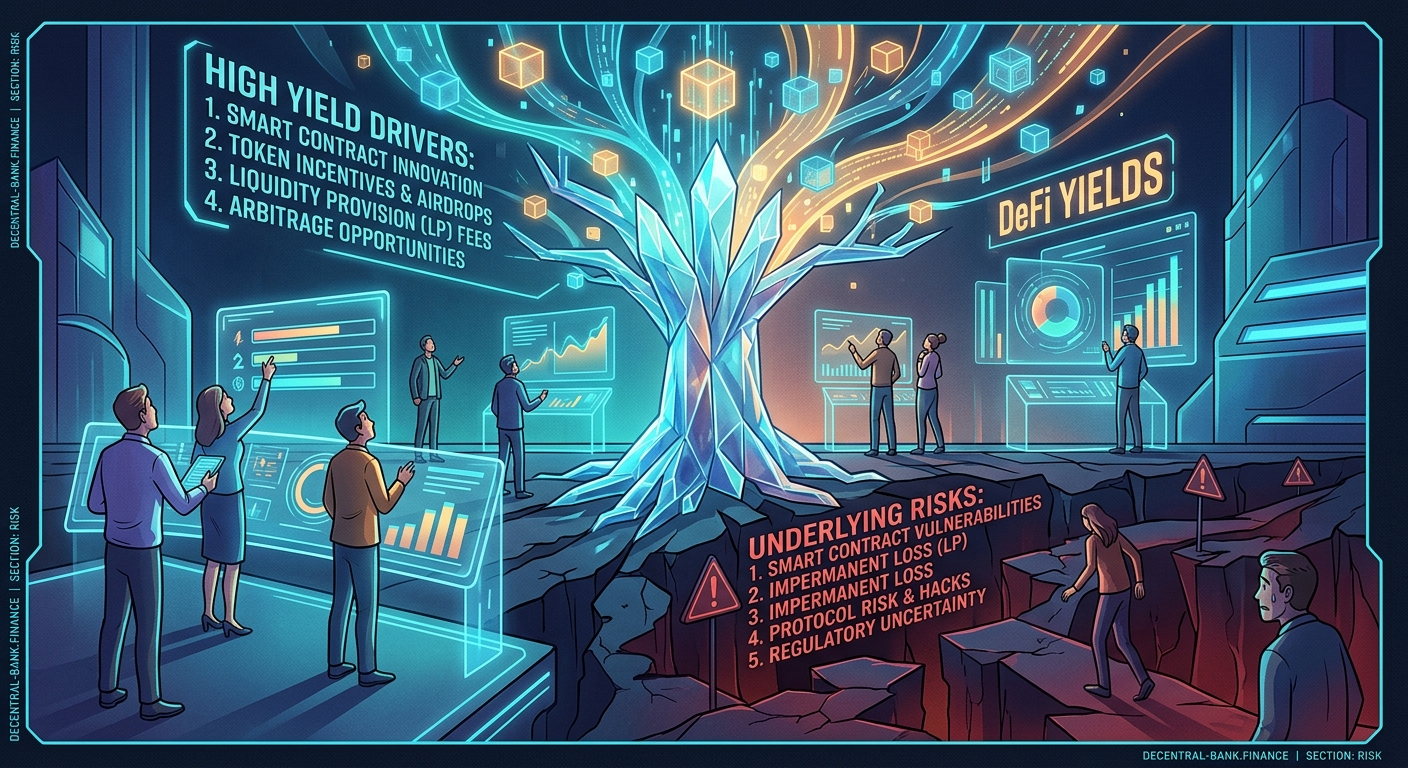

The real risks hiding behind high APY numbers

Traditional finance separates your risk tolerance from your return expectations through regulation and insurance.

DeFi doesn’t.

Every percentage point above “risk-free” rates represents actual danger to your capital. Here’s what you’re actually accepting when you chase high yields.

Smart contract vulnerabilities can drain everything

Your funds sit in code, not a vault.

If that code has a bug, hackers can exploit it. They’ve done it repeatedly, stealing billions from protocols that passed audits.

Smart contract audits reduce risk but don’t eliminate it. Auditors miss bugs. New attack vectors emerge. Protocols combine in ways that create unexpected vulnerabilities.

One exploit can empty the entire protocol overnight. Insurance exists but doesn’t cover most losses.

Your 12% APY compensates for this code risk. Banks don’t have this problem because your deposits sit in regulated institutions with FDIC insurance.

Liquidation risk in lending protocols

Borrowing in DeFi requires over-collateralization.

You deposit $150 worth of ETH to borrow $100 in stablecoins. If ETH’s price drops, the protocol automatically liquidates your collateral to protect lenders.

This happens fast during market crashes. You can lose everything while sleeping.

Understanding collateral ratios helps, but volatility can outpace your ability to add collateral. High lending rates compensate lenders for borrowers who get liquidated at a loss during extreme moves.

Stablecoin de-pegging destroys yield calculations

Most DeFi yields are denominated in stablecoins.

Earning 10% APY in USDC sounds great until USDC drops to $0.92. Your actual return in dollar terms just went negative.

Stablecoin de-pegging has happened to major stablecoins. UST collapsed completely. USDC temporarily broke its peg during the Silicon Valley Bank crisis.

You’re not just earning yield. You’re betting the stablecoin maintains its peg.

How different DeFi strategies generate different yields

Not all DeFi yields come from the same source. Understanding the mechanism helps you assess actual risk.

| Strategy | Typical APY | Primary Risk | Return Source |

|---|---|---|---|

| Stablecoin lending | 3-8% | Smart contract exploit, de-pegging | Borrower interest payments |

| Liquidity provision | 5-30% | Impermanent loss, smart contract risk | Trading fees, token rewards |

| Staking | 4-12% | Slashing, lock-up periods | Network inflation, transaction fees |

| Yield farming | 20-500% | Token price collapse, rug pulls | Token emissions, multiple fee layers |

The table shows a clear pattern: higher yields come with more complex and severe risks.

Stablecoin lending offers the lowest returns because it has the fewest risk factors. You’re still exposed to smart contracts and stablecoin stability, but you avoid impermanent loss and token price volatility.

Yield farming combines every possible risk. You’re exposed to multiple smart contracts, token price movements, impermanent loss, and often rug pull risk from unaudited protocols.

Staking rewards come from network inflation

When you stake tokens on proof-of-stake networks, you’re helping secure the blockchain.

Your rewards come from newly minted tokens and transaction fees. The protocol inflates the token supply to pay stakers.

If the token price doesn’t appreciate faster than inflation, your real return is negative. You’re earning more tokens, but each token is worth less.

Staking rewards after fees and inflation often look less impressive than the headline APY suggests.

Lending yields fluctuate with utilization

Lending rates aren’t fixed.

They rise when borrowing demand increases and fall when supply exceeds demand. A protocol advertising 8% APY today might pay 3% next week.

This variability makes planning difficult. You can’t count on consistent returns like you would with a traditional CD or bond.

Variable vs fixed interest rates in DeFi lending shows how different protocols handle rate stability.

Comparing DeFi yields to traditional finance returns

Banks and DeFi operate on fundamentally different models.

Traditional savings accounts pay low rates because they’re extremely safe. FDIC insurance covers up to $250,000. Banks must follow strict regulations. Your money is liquid and accessible.

DeFi protocols offer higher rates because they transfer risk to you.

No insurance. No regulation. No customer service to call when something breaks. You’re responsible for your own security, from wallet setup to smart contract approvals.

That responsibility commands a premium. The 5-10% gap between bank savings rates and DeFi lending rates represents the value of regulatory protection and institutional guarantees.

Why traditional institutions can’t match DeFi rates

Banks face costs DeFi protocols avoid:

- Physical infrastructure and branches

- Compliance and regulatory reporting

- Deposit insurance premiums

- Employee salaries and benefits

- Shareholder profit expectations

These costs eat into the spread between what banks charge borrowers and pay depositors.

DeFi protocols run on code. Their costs are minimal: smart contract deployment, audits, and core development. Everything else is automated.

The efficiency advantage is real. But it comes with the trade-off of no safety net.

How to evaluate whether a DeFi yield is sustainable

Not every high APY represents a fair risk-reward trade-off.

Some protocols offer unsustainable rates to attract deposits, then collapse when the music stops. Others provide genuinely valuable services that justify their returns.

Here’s how to tell the difference:

-

Identify the revenue source. Where does the yield actually come from? Trading fees and borrowing interest are sustainable. Pure token emissions are not.

-

Check the protocol’s total value locked (TVL). Established protocols with billions in TVL have proven their model. New protocols with tiny TVL are experiments that could fail.

-

Review the audit history. Has the protocol been audited by reputable firms? Have they fixed identified issues? Why audits still miss critical bugs explains limitations, but audited protocols are safer than unaudited ones.

-

Understand the token economics. If rewards come from token emissions, check the emission schedule. Protocols that mint unlimited tokens create hyperinflation that destroys value.

-

Test with small amounts first. Never deposit your entire portfolio into a new protocol. Start small, verify everything works, and scale up gradually.

The best DeFi yields come from protocols with sustainable revenue models, proven security track records, and transparent token economics. If you can’t explain where the yield comes from, you shouldn’t deposit funds.

Common mistakes beginners make chasing high yields

Seeing triple-digit APY numbers triggers FOMO.

You imagine your portfolio doubling in months. You skip research and deposit everything into the highest-yielding pool you can find.

This almost always ends badly.

Ignoring impermanent loss calculations

Liquidity pools advertise high APYs without mentioning impermanent loss.

You deposit $1,000 worth of ETH and USDC into a pool offering 40% APY. ETH’s price doubles. You earned $400 in fees, but you would have made $500 just holding ETH.

You actually lost money compared to holding. The “40% APY” was misleading because it didn’t account for opportunity cost.

Impermanent loss calculators help you understand this before depositing.

Forgetting about gas fees

High yields on small deposits get eaten by transaction costs.

Depositing $100 into a lending protocol might cost $15 in gas fees. Withdrawing costs another $15. You need to earn 30% just to break even.

Ethereum gas fees make DeFi impractical for small amounts. Layer 2 solutions reduce costs but add complexity and additional smart contract risk.

Falling for token emission schemes

New protocols attract users by offering governance tokens as rewards.

The APY looks incredible because they value those tokens at current market prices. But market prices are based on tiny trading volumes with no depth.

When you try to sell your rewards, you discover there are no buyers. The token price crashes 90%. Your “500% APY” becomes a 50% loss.

This happens constantly. Token emission rates determine whether a protocol can sustain its rewards.

Building a safer DeFi yield strategy

You can earn meaningful returns in DeFi without gambling your entire portfolio.

Start with established protocols that have operated for years without major exploits. Aave, Compound, and Uniswap have proven track records.

Accept lower returns in exchange for better security. A sustainable 6% beats a theoretical 60% that evaporates in an exploit.

Diversify across protocols and strategies

Don’t put everything in one protocol, no matter how safe it seems.

Split deposits across multiple platforms. If one gets exploited, you only lose a portion of your capital.

Mix different yield strategies:

- Stablecoin lending for steady, lower-risk returns

- Blue-chip token staking for moderate yields with less smart contract risk

- Small allocations to higher-risk liquidity pools for potential upside

This approach balances risk and return better than going all-in on any single strategy.

Monitor your positions actively

DeFi isn’t passive income.

Protocols change parameters. New risks emerge. Token prices fluctuate. You need to check your positions regularly and adjust when conditions change.

Set price alerts for your collateralized loans. Watch for protocol governance proposals that might affect your deposits. Stay informed about security incidents in the broader ecosystem.

Getting started with DeFi requires ongoing education, not just an initial deposit.

Making informed decisions about DeFi yields

High yields exist in DeFi because real risks exist.

Protocols don’t pay 10% out of generosity. They pay because they need to compensate you for smart contract risk, liquidation exposure, impermanent loss, and regulatory uncertainty.

Understanding why DeFi yields are so high helps you evaluate whether specific opportunities match your risk tolerance. Some people gladly accept smart contract risk for extra returns. Others prefer the security of traditional finance.

Neither choice is wrong. The mistake is chasing yields without understanding where they come from and what could go wrong.

Start small. Learn the mechanisms. Test protocols with amounts you can afford to lose. Build knowledge before scaling up.

DeFi offers genuine opportunities for better returns than traditional finance. But those opportunities come with responsibilities that banks handle for you. Your job is to decide whether the extra yield justifies the extra work and risk.