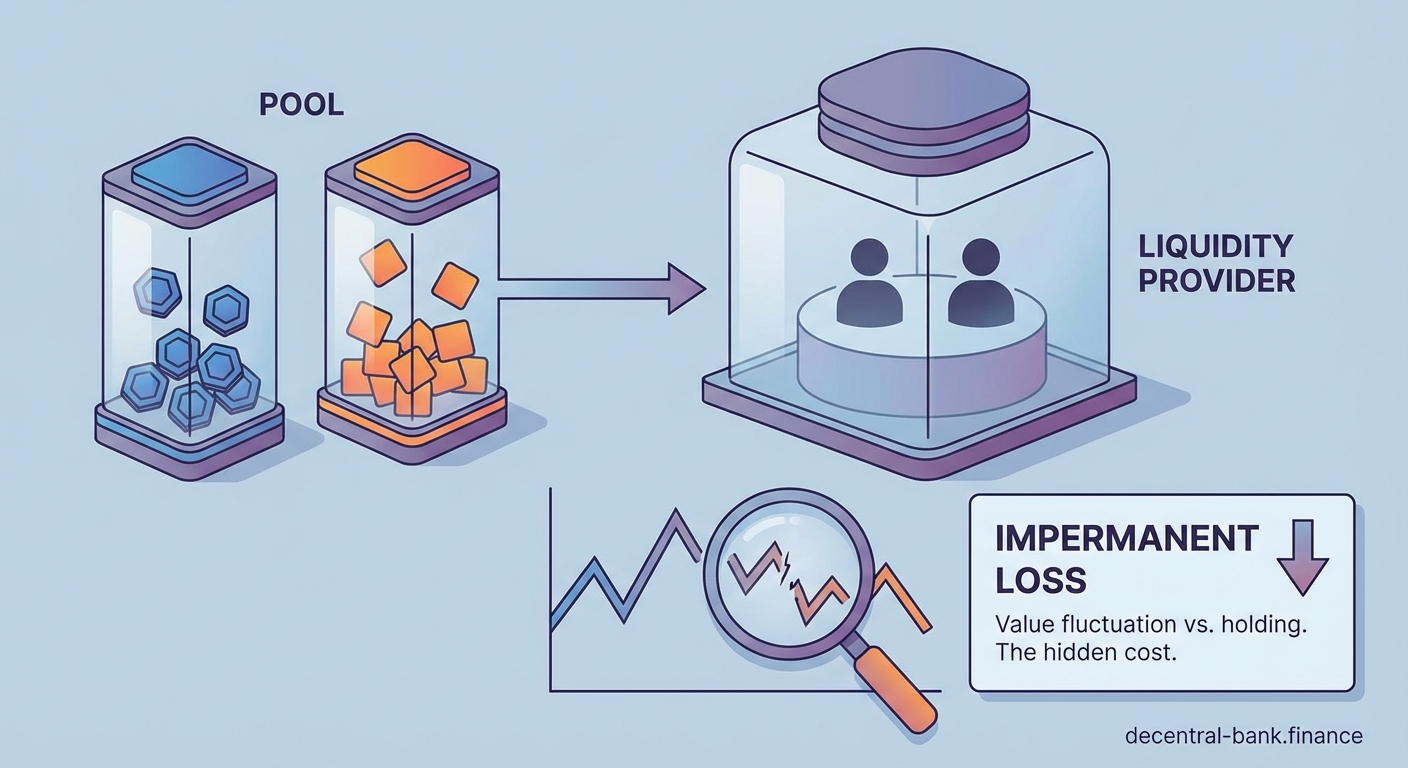

Providing liquidity on decentralized exchanges sounds like easy passive income. You deposit two tokens into a pool, earn trading fees, and watch your balance grow. But there’s a catch that catches most people off guard. When token prices shift, you might end up with less value than if you’d just held your assets. That’s impermanent loss, and it’s the single biggest risk facing liquidity providers today.

Impermanent loss occurs when the price ratio between two tokens in a liquidity pool changes after you deposit them. The automated market maker rebalances your position, leaving you with less total value compared to simply holding those tokens in your wallet. Understanding how this mechanism works helps you choose better pools and protect your capital from unexpected losses.

What causes impermanent loss in liquidity pools

When you add liquidity to a decentralized exchange like Uniswap, you’re depositing equal values of two tokens. Let’s say you put in $1,000 of ETH and $1,000 of USDC when ETH is worth $2,000. You now own a share of that pool.

Here’s where things get tricky. The pool uses a constant product formula to maintain balance. When traders buy ETH from the pool, the price of ETH in that pool rises. The algorithm automatically adjusts the ratio of tokens to keep the product constant.

This rebalancing happens without your input. The pool sells some of your rising asset and buys more of the falling asset. It’s doing the exact opposite of what a smart trader would do.

The loss is called “impermanent” because it only becomes permanent when you withdraw. If prices return to their original ratio, the loss disappears. But in reality, prices rarely revert perfectly. Most liquidity providers lock in their losses when they exit.

The math behind this isn’t complicated. When one token doubles in price relative to the other, you’ll experience roughly 5.7% impermanent loss. If one token triples, that loss jumps to about 13.4%. The bigger the price divergence, the worse your position becomes.

How to calculate your actual loss step by step

Understanding the numbers helps you make better decisions. Here’s how to calculate impermanent loss for any position:

- Record the exact price ratio of both tokens when you entered the pool.

- Check the current price ratio of those same tokens.

- Calculate what your holdings would be worth if you’d simply held them in your wallet instead of providing liquidity.

- Compare that value to your current pool position value.

- Subtract your pool value from your hold value to find your impermanent loss.

Let’s work through a real example. You deposited 1 ETH ($2,000) and 2,000 USDC when ETH was $2,000. Your total position was worth $4,000.

Now ETH has risen to $3,000. If you’d just held those tokens, you’d have $5,000 total (1 ETH at $3,000 plus 2,000 USDC).

But in the pool, the algorithm rebalanced your position. You now have approximately 0.816 ETH and 2,449 USDC. That’s worth $4,898 total.

Your impermanent loss is $102, or about 2% of what you would have had by holding. And that’s before counting any trading fees you earned.

Why price volatility amplifies your risk

Stable pairs experience minimal impermanent loss. A USDC/DAI pool barely moves because both tokens track the dollar. Your biggest risk there is a depeg event, not normal price movement.

Volatile pairs are where impermanent loss becomes painful. ETH/USDC pools see constant rebalancing as ETH swings up and down. The more volatile the pair, the more the algorithm trades against your position.

Correlated assets offer a middle ground. ETH/stETH pools have lower impermanent loss because both tokens tend to move together. When ETH rises, stETH usually follows. The price ratio stays relatively stable.

Choose your pools based on price correlation, not just APY. A 200% yield on a volatile pair can easily be wiped out by impermanent loss, while a 20% yield on a stable pair might actually put money in your pocket.

Concentrated liquidity amplifies everything. Uniswap V3 lets you provide liquidity within specific price ranges. This boosts your fee earnings but also magnifies impermanent loss. If the price moves outside your range, you stop earning fees entirely and your loss accelerates.

Common mistakes that make impermanent loss worse

| Mistake | Why it hurts | Better approach |

|---|---|---|

| Chasing high APY pools | Usually signals extreme volatility or low liquidity | Focus on established pairs with moderate returns |

| Providing liquidity to meme tokens | Price can crash 90% overnight | Stick to assets with real utility and liquidity |

| Ignoring fee tier selection | Wrong tier means less competitive position | Match fee tier to pair volatility |

| Setting tight ranges on V3 | Price moves out of range frequently | Use wider ranges unless actively managing |

| Forgetting about gas costs | Multiple rebalances eat into profits | Calculate total costs before entering position |

Many providers make the mistake of treating liquidity provision like staking. Staking is relatively passive. Liquidity provision requires active monitoring and strategy.

Another common error is providing liquidity to both sides of a trade you’re already making. If you’re bullish on ETH, providing ETH/USDC liquidity forces you to sell ETH as it rises. You’re working against your own thesis.

Some people try to offset impermanent loss by choosing pools with governance token rewards. But those tokens often drop in value faster than you can earn them. You end up with impermanent loss plus a bag of depreciating tokens.

Practical strategies to minimize your losses

Start with stablecoin pairs if you’re new to liquidity provision. USDC/USDT or DAI/USDC pools have minimal impermanent loss. You won’t get rich on the fees, but you won’t lose principal either.

Consider single-sided liquidity options. Some protocols let you provide just one token while they handle the pairing. You avoid impermanent loss but typically earn lower fees.

Use liquidity provision as a selling strategy. If you plan to take profits on a rising asset anyway, providing liquidity automates that process. The pool sells your asset as it rises, which might align with your goals.

Time your entries and exits around major price movements. Enter pools when you expect prices to stay relatively stable. Exit before anticipated volatility like major protocol upgrades or macroeconomic events.

Here are specific tactics that work:

- Provide liquidity to pairs where you’re neutral on both assets

- Choose correlated pairs like ETH/WBTC where prices tend to move together

- Use concentrated liquidity only if you can monitor and rebalance daily

- Calculate your break-even point where trading fees offset impermanent loss

- Set price alerts so you know when to exit before losses accelerate

Understanding how DeFi actually works helps you see why these mechanisms exist. Automated market makers need liquidity providers to function, but they’re designed to benefit traders, not necessarily providers.

When trading fees actually compensate for losses

Fee income is your main defense against impermanent loss. High-volume pools generate more fees, which can offset price divergence losses.

The 0.3% fee tier on Uniswap works well for moderately volatile pairs. ETH/USDC sees enough volume that providers often earn back their impermanent loss within days or weeks.

The 1% fee tier suits more exotic or volatile pairs. Lower volume means you need higher fees per trade to compensate for increased impermanent loss risk.

The 0.05% tier is for stable pairs where impermanent loss is minimal. High volume on these pairs can generate solid returns with almost no price risk.

Calculate your daily fee earnings and compare them to your current impermanent loss. If fees are accumulating faster than your loss is growing, you’re in good shape. If impermanent loss is outpacing fees, consider exiting.

Some pools never generate enough fees to justify the risk. Newly launched tokens or low-volume pairs might advertise high APYs through token rewards, but actual trading fees are negligible. Without real fee income, you’re just gambling on token prices.

Advanced techniques for active liquidity managers

Range orders on Uniswap V3 let you provide liquidity in a tight band just above or below current price. This mimics a limit order. When price moves through your range, you effectively sell one asset for another while earning fees.

Multiple positions across different ranges spread your risk. Instead of one concentrated position, create three or four positions at different price levels. This ensures you’re always earning fees somewhere.

Rebalancing strategies involve moving your liquidity as prices shift. This requires active management and gas fees, but it keeps you in optimal earning ranges. Only worth it if you have significant capital and low gas costs.

Hedging with options or perpetual futures can offset impermanent loss. If you’re providing ETH/USDC liquidity and ETH rises, your short position profits while your pool position loses. The gains and losses offset each other.

Some protocols offer impermanent loss protection. Bancor pioneered this approach, gradually increasing your protection the longer you stay in a pool. After 100 days, you’re fully protected against impermanent loss. The catch is you must stay that long and the protocol must remain solvent.

Real examples of impermanent loss in action

During the 2021 bull run, many ETH/USDC providers watched ETH climb from $1,000 to $4,000. Their pool positions grew in value, but they would have made far more by simply holding ETH.

Someone who provided $10,000 of liquidity ($5,000 ETH, $5,000 USDC) at $1,000 ETH ended up with roughly $15,800 when ETH hit $4,000. Sounds great until you realize holding would have given them $17,500. They lost $1,700 to impermanent loss.

The fees they earned during that period might have been $500 to $1,000, depending on volume. Still a net loss compared to holding, even though their dollar value increased.

Stablecoin providers had the opposite experience. USDC/DAI liquidity providers earned steady fees with almost zero impermanent loss. A $10,000 position might have earned $800 in fees over the same period with minimal price risk.

The Luna/UST collapse showed the worst-case scenario. Providers in UST pools lost everything as UST depegged and crashed. Impermanent loss was the least of their problems. This highlights why understanding the underlying assets matters more than chasing yields.

How pool structure affects your risk exposure

50/50 pools are standard on most DEXs. You provide equal values of both tokens. This creates symmetrical impermanent loss risk in both directions.

Weighted pools like those on Balancer let you choose different ratios. An 80/20 ETH/USDC pool gives you more ETH exposure and less impermanent loss if ETH rises. But you’ll have worse impermanent loss if ETH falls.

Stable swap pools use different math optimized for assets that should trade near 1:1. These pools have much lower impermanent loss but only work for correlated assets.

Dynamic fee pools adjust trading fees based on volatility. When prices swing wildly, fees increase to compensate providers for higher impermanent loss risk.

Understanding these structures helps you match your risk tolerance to the right pool type. Conservative providers stick to stable swaps. Aggressive providers use concentrated liquidity on volatile pairs.

Tools and calculators you should be using

Impermanent loss calculators show your potential loss at different price ratios. Input your entry prices and current prices to see exactly where you stand.

APY calculators factor in both fee earnings and impermanent loss to show your true return. Many pools advertise high APYs that don’t account for price divergence.

Position trackers monitor your liquidity across multiple protocols. They alert you when impermanent loss exceeds certain thresholds or when you drift out of range on V3 positions.

Analytics platforms like Dune Analytics show historical fee earnings for specific pools. This helps you estimate whether fee income will offset your impermanent loss over time.

Portfolio trackers designed for DeFi show your total position value including unclaimed fees. Regular wallet trackers often miss these details, giving you an incomplete picture.

Tax implications you need to consider

Every rebalance inside the pool creates a taxable event in most jurisdictions. The algorithm is constantly trading your tokens, even though you’re not actively doing anything.

When you withdraw liquidity, you’re likely receiving different amounts of each token than you deposited. This creates capital gains or losses that you must report.

Fee earnings are typically treated as income, not capital gains. This means higher tax rates on your fee earnings compared to long-term holdings.

Tracking all these transactions manually is nearly impossible. You need specialized crypto tax software that can parse DEX transactions and calculate your actual tax liability.

Some providers are shocked to discover they owe taxes on positions that lost money overall. You might have impermanent loss that exceeded your fee earnings, but the fee earnings are still taxable income.

Security risks beyond impermanent loss

Smart contract bugs can drain entire liquidity pools. Even audited contracts sometimes have vulnerabilities that hackers exploit.

Oracle manipulation can cause artificial price swings that trigger massive impermanent loss. Attackers manipulate price feeds to profit at the expense of liquidity providers.

Rug pulls on new tokens leave you holding worthless assets. The project team dumps their tokens, price crashes, and your pool position becomes nearly worthless.

Protocol governance changes can alter fee structures or introduce new risks. What looked like a safe pool today might become risky after a governance vote.

Front-running bots can extract value from your position through sandwich attacks. They manipulate prices around your transactions to profit at your expense.

These risks stack on top of impermanent loss. A pool with minimal impermanent loss risk might still be dangerous if the underlying protocol has security issues.

Making smarter decisions about liquidity provision

Impermanent loss isn’t inherently bad. It’s a trade-off. You accept price divergence risk in exchange for fee income and potential token rewards.

The key is understanding when that trade makes sense. Providing liquidity to stable pairs with high volume is often profitable. Providing liquidity to volatile meme tokens rarely works out.

Calculate your break-even point before entering any pool. How much in fees do you need to earn to offset expected impermanent loss? If the math doesn’t work, don’t provide liquidity.

Consider your overall portfolio strategy. If you’re already long on both assets in a pool, providing liquidity might reduce your risk by automatically taking profits. If you’re bullish on one asset, providing liquidity works against you.

Monitor your positions regularly. Impermanent loss that’s acceptable today might become unacceptable tomorrow. Set clear exit criteria before you enter.

Your next steps as a liquidity provider

Start small with stablecoin pairs to understand the mechanics without risking significant capital. Watch how fees accumulate and how small price movements affect your position.

Move to correlated pairs like ETH/WBTC once you’re comfortable. These offer higher yields than stablecoins with manageable impermanent loss risk.

Only use concentrated liquidity after you’ve mastered standard pools. The complexity and risk aren’t worth it unless you can actively manage your positions.

Keep detailed records of every position, entry price, exit price, and fee earnings. You’ll need this for taxes and to evaluate whether liquidity provision makes sense for you.

Remember that impermanent loss is just one factor. Protocol security, gas costs, opportunity cost, and your own time investment all matter. Sometimes the best decision is to skip liquidity provision entirely and focus on simpler strategies.

The DeFi ecosystem needs liquidity providers to function, but that doesn’t mean you need to be one. Understand the risks, do the math, and make informed decisions based on your specific situation and goals.